PRM & GLV’s well is ranked amongst highest impact wells of 2022

Published 22-APR-2022 10:31 A.M.

|

11 minute read

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 7,000,000 GLV shares, 49,000,000 PRM shares and 11,833,332 PRM options at the time of publishing this article. The Company has been engaged by PRM and GLV to share our commentary on the progress of our investment in PRM and GLV over time.

Last week we launched two new investments in our Catalyst Hunter portfolio, Prominence Energy (ASX: PRM) and Global Oil and Gas (ASX:GLV).

Together, they have 37.5% interest in the Sasanof Prospect located in the North West Shelf, offshore WA, where drilling is set to take place in just weeks.

The Sasanof Prospect has a prospective resource of 7.2 trillion cubic feet and 176 million barrels of condensate on a 2U basis (unrisked mid case).

It is surrounded by giant gas fields - the North West shelf is home to ~47mtpa of liquefied natural gas (LNG) processing infrastructructure and some of Australia’s biggest ever gas discoveries.

PRM holds 12.5% interest and GLV a 25% interest in the Sasanof Prospect.

The prospect will be tested via the drilling of the Sasanof-1 well, which is expected to begin sometime in the week of 9th–16th May.

The prospect has the potential to host a resource larger than, or at least rival, the size of discoveries made by oil and gas majors like Exxon, Chevron and Woodside in this part of WA.

For some context, the Bass Strait, offshore Victoria, has been the biggest source of gas supply domestically, and had peak reserves of ~10 trillion cubic feet.

PRM and GLV therefore have exposure to one of the biggest ever drilling events done by an ASX listed junior in recent decades.

We have decided to invest in both stocks.

NOTE: Investing in high impact oil & gas exploration wells so close to spud date is very high risk and the result of drilling will be near term and binary. The result will be known in the next two months, and depending on the result we expect the share price could rise OR FALL significantly.

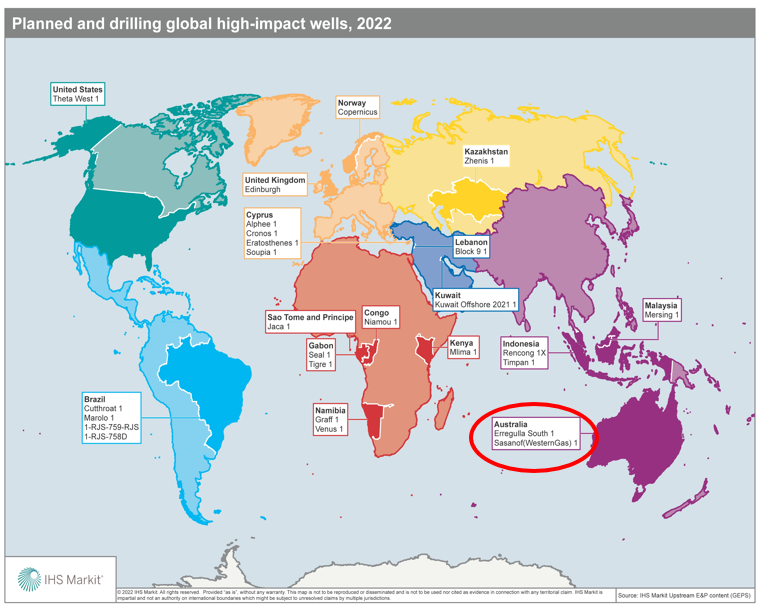

While we wait for drilling to begin, we spent some time looking at what other high impact wells are going to be drilled over the course of 2022.

S&P Global included the Sasanof-1 well in its 2022 “High impact well report” in early January ranking it amongst some of the biggest drilling events being done this year.

Importantly, we get to find out whether or not that prospective resource can be converted into a proven discovery very soon, with the Sasanof-1 well scheduled for spudding in mid-May.

This means the major catalyst is now less than 3 weeks away.

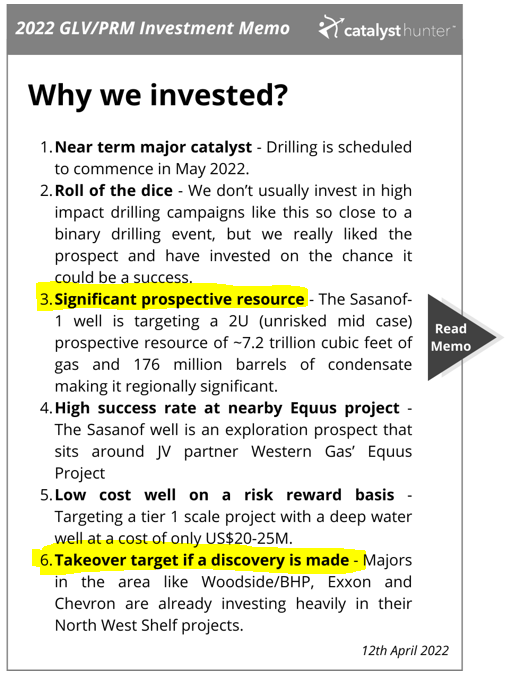

Below is a screenshot from our 2022 PRM/GLV Investment Memo summary of the summary of the key reasons why we invested in both PRM and GLV.

We listed the near term major catalyst as one of the key reasons why we invested in both PRM and GLV, along with 5 other key reasons.

The focus of today’s deep dive will be on the following two:

- Reason no. 3 = Significant prospective resource

- Reason no. 6 = Takeover target if a discovery is made

What makes the Sasanof prospect a “high impact well”?

When referring to “high impact wells”, the reference is generally made with respect to the size of the prospect being drilled.

For example, a 10 trillion cubic feet (Tcf) prospective resource might be drilled and a discovery is made with a 2 Tcf reserve number, that discovery is still extremely large when all things are considered and is likely to be considered economic.

🎓 = To learn more about how to read oil and gas resources, and the differences between prospective resources and reserves, check out our educational article here.

S&P global’s report of 2021 “high impact wells” summarises this perfectly with the following quote, “A total of 32 “high impact wells” were spudded in 2021 with approximately two-thirds making discoveries of varying size”.

Two thirds is a high hit rate when it comes to exploration, so clearly when it comes to oil and gas drilling the size of a target really does matter.

S&P Global also estimated that in 2022, 20 high impact wells were planned to be drilled, one of those being PRM & GLV’s Sasanof-1 well, which is targeting a giant prospective resource of:

- 17.8 trillion cubic feet and 449 Million barrels of condensate on a 3U basis (high case)

AND

- 7.2 trillion cubic feet and 176 million barrels of condensate on a 2U basis (mid case).

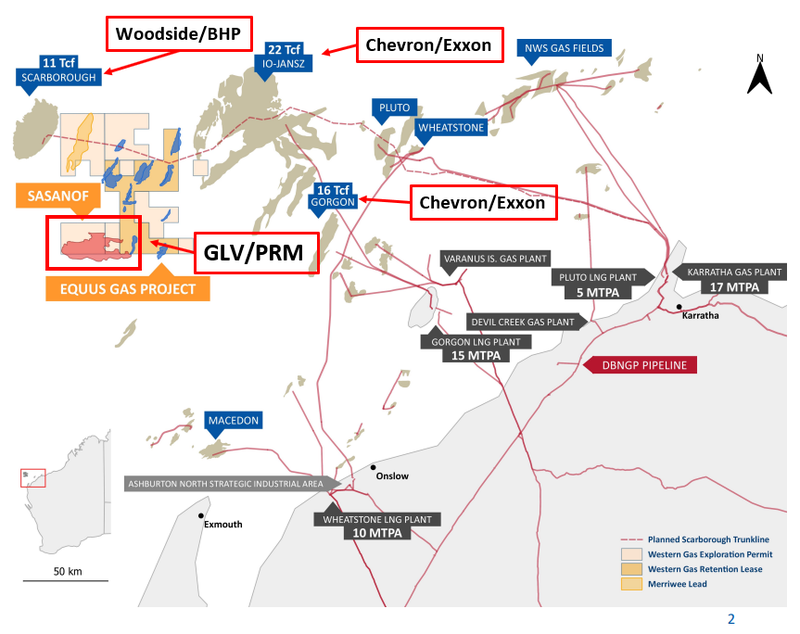

Importantly, the Sasanof Prospect sits in a part of the world where these mega discoveries have been made before being surrounded by:

- 22 Tcf Jansz and 16 Tcf Gorgon discoveries made by oil and gas supermajors Chevron and Exxon. (Interestingly the Greater Gorgon Project which combines these two projects is the largest oil & gas project in Australian history).

- 11 Tcf Scarborough discovery which is being developed via a JV between Woodside and BHP, which is spending over $16 billion to develop the asset.

PRM and GLV’s Sasanof prospect sits right in between the three of these projects.

Putting this all together, PRM and GLV hold an interest in a project that has significant scale with the potential to host a resource larger than, or at least rival the size of, discoveries made by oil and gas majors like Exxon, Chevron and Woodside in this part of WA.

As a result, it can be classified as a “high impact well” and one of the biggest ever drilling programs we have seen an ASX listed junior do in recent decades.

These type opportunities very rarely end up in the hands of juniors, with projects in the trillions of cubic feet potential generally ending up in the hands of oil and gas supermajors.

Looking at the North West Shelf, the mega projects are owned by the following majors:

Scarborough (11 Tcf resource): Woodside Petroleum (capped at A$32 billion) and BHP (capped at A$265 billion)

Jo-Jansz (22 Tcf resource) + Gorgon (16 Tcf resource): Majority owned by Chevron (capped at US$340 billion, ExxonMobil (capped at US$372 billion) and Shell (capped at US$220 billion).

All of these are owned by companies with market caps in the billions, with the balance sheet power to drill and develop these size projects.

Our investments on the other hand are trading at low market caps which leaves plenty of room for a re-rate in the event a successful discovery is made.

PRM currently trades at a market cap of $31M with its 12.5% interest in the project, while GLV trades at a market cap of $64M with a 25% interest in the project.

Of course, the reason they trade at these market caps is because there is no confirmed discovery yet and as with any exploration prospect, there is always a chance no discovery is made and the stocks could go down sharply on failure.

RISK NOTE**We highlight the main “exploration risk” in the risks section of our 2022 Sasanof Investment Memo which can be viewed here.

Takeover target if a discovery is made

Having established the scale of the target PRM and GLV are drilling, it's important to try and put some context around what a “success” case looks like for the upcoming drilling program.

The ultimate aim is to make a discovery and projects like Sasanof, take a significant amount of preparation and capital. A successful discovery should attract the attention of an oil & gas supermajor who either takes over the prospect in full, or decides to farm-in an interest in the project.

We think the interest will come because of the size and location of the Sasanof project:

Remember that map above - the Sasanof Prospect sits right in between Woodside/BHP’s Scarborough development and the Greater Gorgon Project owned by Chevron/Exxon/Shell.

The Greater Gorgon Project is the largest project ever developed in Australian history and is home to one of the worlds largest liquefied natural gas (LNG) processing facilities. The North West Shelf is also home to ~47mtpa of total LNG processing capacity.

The significance is that the gas discovered and produced in this region can be processed and then shipped all across the world in the form of LNG, as well as supplying domestic gas markets.

This means the projects are considered in the global context and not just from a domestic Australian perspective.

In turn, the project's global scale will mean that if a successful discovery is made, the project will pop up on the radars of the same supermajors operating in the area (Exxon/Chevron/Shell) who are looking to make bolt-on acquisitions.

Instead of having to go off and make a new discovery, these supermajors could just take over the Sasanof Project and tie it into their existing pipeline/processing infrastructure.

Or, this project could be large enough for a new energy supermajor to enter the NW Shelf.

A successful discovery could be large enough to be a “starter” asset for a supermajor that doesn't have exposure in Australia.

A major could come in, take the project over and then build out its Australian energy portfolio off of the Sasanof Project.

This all means that a successful discovery at Sasanof could stack up as a takeover opportunity both economically and strategically in the case of a “starter asset” for a supermajor.

Some of those majors without exposure to this area are BP (capped at US$102 billion) and Total (capped at US$133M). Both these companies had in excess of US$20 billion in cash on hand each as of 31/12/2021 meaning the right acquisition opportunity would be easy for them to finance.

We have seen this type of takeover happen before...

In 2018, junior WA gas explorer AWE was acquired by US$42 billion Japanese conglomerate Mitsui in a $602M takeover.

The takeover came after AWE made the Waitsia discovery in 2014, in what it called the largest onshore discovery in Australia in the last 50 years.

AWE’s project had a net 2P resource of 410 petajoules (388 billion cubic feet), valuing the transaction at ~$1.5M per BCF of gas resource.

Taking the mid-case prospective resource of 7.2 trillion cubic feet and 176 million barrels of condensate on a 2U basis (mid case), the Sasanof-1 well will be targeting a prospective resource almost 18x the size of AWE’s proven resource number.

Using the $1.5M per BCF of proven resource number, Sasanof would have a value of $11 billion (if it comes in).

The obvious caveat here is that AWE’s discovery had gone through the drilling process, the discovery had been confirmed and the resource was upgraded into the proven category.

🎓 = To learn more about how to read oil and gas resources, check out our educational article here.

The Sasanof Prospect is still at the prospective stage, and we suspect that even in the case of a successful discovery being made the proven resource would likely be much lower than that of the prospective figure.

Another caveat is that AWE’s project was also an onshore project, whereas the Sasanof Project is offshore and would cost more to actually bring into production.

It's worth noting these are rough calcs that should never be used as a basis to make an investment decision. We like to do this type of comparison just to get an idea of whether or not the absolute best case scenario is worth drilling for.

I.e. if the Sasanof Prospect at its absolute best case could be worth $10M, but had to spend $40M to get there, we would immediately pass on the opportunity.

It's also worth noting that an in ground value of any discovery is based on a myriad of assumptions that can change based on a number of factors.

To summarise, should a successful discovery be made:

- The Sasanof Prospect has sufficient scale and is in the right part of Australia/World, surrounded by LNG processing capacity, to make it the ideal takeover target for oil and gas majors with and without exposure to Australian gas projects.

- There is a history of international interest in Australian gas projects with the $602m takeover of AWE in 2018 by US$42 billion Japanese conglomerate Mitsui.

If the drilling program delivers a discovery, we expect that interest in the project will come from all around the world.

Our investments, PRM and GLV, will proportionately share in the risks and rewards of the drilling program with a combined 37.5% interest in whatever takeover offer may be received.

PRM will own 12.5% of the project and GLV will own 25%.

RISK CAUTION** All of this discussion is assuming a successful discovery is made. There is always a risk that the Sasanof-1 well returns nothing and in that case all of these factors would be considered invalid.

Our investment plan

Our investments in PRM & GLV will have a different investment strategy versus what we are used to.

We see this as high risk, high reward investment, with the big result due very soon.

This is a binary event - it could go either way.

We have <2% of our portfolio invested in this and know that there is a risk that should the drilling program find nothing, the majority of our investment could be wiped out.

Below is our investment plan as per our 2022 Investment Memo, to see our detailed breakdown check out our initiation note from last week here.

Our 2022 PRM/GLV Investment Memo

Below is our 2022 Investment Memo for PRM and GLV where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the memo is to track the progress of our portfolio companies using our Investment Memo as a benchmark, throughout 2022.

In our PRM/GLV Investment Memo you’ll find:

- Key objectives for PRM/GLV in 2022

- Why we continue to hold PRM/GLV

- What the key risks to our investment thesis are

- Our investment plan

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.