VUL Withstands Short Seller Attack

The attempted short seller attack on Friday last week targeting Vulcan Energy Resources (ASX:VUL) was the biggest story in our portfolio, gaining a lot of online and media attention.

We shared our theory and workings on why we thought that IF the VUL share price opened at above $13.50 then the 1,290,385 shorted VUL shares might need to be quickly purchased back, putting upward pressure on the VUL share price - today we provide our analysis of what happened on the day.

While the VUL share price didn’t open above the $13.50 that we calculated could trigger a "short squeeze", we believe that Friday’s short attack will be considered a "failure" by the short sellers with the VUL share price holding up very well at an average of $12.75 for the day, giving up just the last 7 days of gains.

Any traders that were looking for the short squeeze would likely have entered at $12.08 on the opening match, and sold into what we suspect was short covering in the following 60 seconds after open as the price ran to $12.80 or into the daily average at $12.75 - more detailed analysis below.

What is VUL and its "Zero Carbon Lithium"?

VUL is developing the world’s first Zero Carbon Lithium Project to target the surging demand in ethical and sustainable lithium for electric vehicle batteries.

VUL plans to produce sustainable battery-grade lithium hydroxide from geothermal brines pumped from wells with a renewable geothermal energy by-product.

VUL’s project is located in Germany, the global heart of the auto industry, in Europe which is leading the world’s charge in decarbonisation and the electrification of their vehicle fleet.

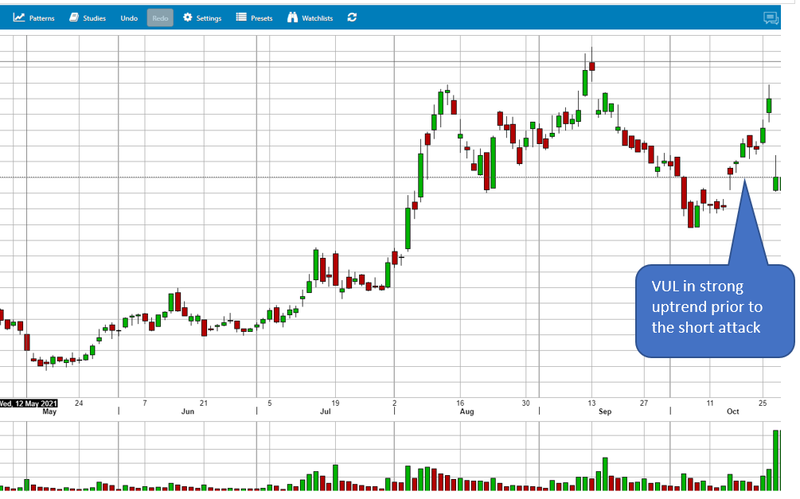

We have been invested in VUL for over two years and initiated our coverage on Wise-Owl at 36c in June 2020 - since then VUL has had a stellar run to touch highs of over $16 after signing three offtake agreements while the lithium price continues to hit new highs each week.

We believe the short attackers thought that the VUL share price had risen too strongly and it made a good target for a short attack, BUT with the world now going green, there are trillions of dollars in investment capital looking to park in a limited number of green and sustainable projects, and companies like VUL will attract a premium, especially as they continue to de-risk their project.

The lithium price hit has just hit another record of US $27 per kg.

World leaders are meeting right now at the COP24 climate conference in Glasgow to lock in decarbonisation commitments, targets and actions.

Alster Research this morning reaffirmed it’s BUY recommendation on VUL with a $22 share price target, in light of the short seller report.

So what happened in last week’s short attack and VUL?

Short sellers (who profit when a share price goes down) took a "short position" in VUL and commissioned an extremely negative report to try and push the VUL price down, so they could increase their gains.

VUL went into a trading halt and released a detailed rebuttal to the disinformation published in the short attack report - Friday was the first session that VUL traded AFTER the short attack report release, and we assume it was THE CRITICAL DAY for the short sellers to make all their profits.

We shared our theory and workings on why we thought that IF the VUL share price opened at above $13.50 then the 1,290,385 shorted VUL shares would be showing a loss and likely be forced to be purchased back on market, pushing the VUL price upwards and generating a "short squeeze" as more and more short positions would need to be covered as the VUL share price started rising, compounding the price rise.

You can see our full workings, including facts, assumptions and links to supporting data in Friday’s commentary.

While VUL didn’t open above the $13.50 where we calculated the shorters would be showing a loss (and be forced to cover), the share price held up very well, trading at a weighted average of ~$12.70 for the day and closing at $12.51, back to where it was last week, giving back just 7 trading sessions worth of gains.

After a big build up during the week, all VUL shareholders must have been watching the market open very closely on Friday, alongside plenty of non-holders who just grabbed the popcorn to see what would happen after the short attack report had made it into mainstream media.

10am finally came and with everyone on the edge of their seats the market was about to open - the VUL bid and offer were loaded on each side when the market starting gun fired...

At 10:09:14 AM VUL opened and 565,508 shares of VUL traded at $12.08 (for $6.83M) on the opening match - the sellers at open were likely shareholders who had been scared by the short seller report.

So while the share price didn’t open at above the $13.50 required for our short squeeze theory to kick in, our assumption remained that the short sellers would cover on the first day the market opened after the short attack report was released where maximum fear and uncertainty was likely in the market, and we assume the short sellers quickly started buying up VUL stock to "cover" and lock in their "gains".

So by our assumptions, at market open a chunk of the open short position could have been covered (ie: shorted shares bought back) at $12.08 for a profit of about $1.42 per share (IF the short sellers covered on the opening match).

Within 60 seconds of open a further $2.78M shares changed hands, with buyers kicking in to push the price up to $12.80 in the first minute - this fast price rise after open looked to have all the hallmarks of short covering during "peak fear", but we don’t have access to the data to confirm it.

For the rest of the day VUL bounced between $12.50 and $13.20 and on record volume, the volume weighted average price for the day was $12.70 - so theoretically the short sellers could have covered and made a profit of around 75c per share if they covered gradually throughout the day.

So if 1,290,385 shorted VUL shares were covered on the day (assuming the short price was around the ~$13.50 we calculated) the short sellers could have made around $928k profit - not including the cost to commission the J Capital report (which we understand costs about $200k) and the costs to create the short facility.

Our final observation was that on the closing match (between 4:00pm and 4:11pm) a total of $22M worth of VUL shares changed hands - this is more than the average daily trading volume of VUL .

While there was obviously a lot of selling, as always there were buyers on the other side of every sell, happy to buy at ~$12.70, and with a total of $115M traded during the day it seems VUL might now have some fresh new shareholder’s on the register at ~$12.70 who are ready to join us and other existing holders on the next leg of the VUL journey.

We will find out how much of the VUL short position was actually covered mid this week when the Friday 29th October "short position" numbers are released - You can see the current daily short positions on any ASX stock here - there is a 4 day delay in short positions being published.

It will be interesting to see how many VUL short positions were closed on Friday. VUL was in a strong upward trend on the back of their third offtake agreement, so we’ll be surprised if most of the short positions weren’t closed on Friday to mitigate the "risk" of VUL’s strong upward trend continuing, especially now that the short sellers "low hanging fruit" of easily scare-able shareholders have been shaken out and a solid new base formed at $12.70 on $115M volume.

So while the opening share price condition of $13.50 for the short squeeze we predicted was not met, we do think the short sellers were probably a little disappointed in the result that their short attack achieved, after VUL held up pretty well above $12.50, giving back just 7 days worth of recent gains.

So VUL weathered the "short attack" storm, and while short attacks can be frustrating for long term shareholders and a distraction for company management, they are unfortunately a part of what happens when a company shows some early success and increased profile like VUL has done over the last 12 months.

On the plus side, a short attack is a good test of the overall robustness of a company and VUL withstood the brunt of this attack, any VUL holders that were planning to sell probably did it yesterday, which means we will have a stronger register going forward.

Finally, a short attack report provides a good reminder and opportunity for shareholders to refresh their due diligence on the company. We continue to hold a long term position in VUL.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.