NTI’s two clinical trial results are in - Treatment success for BOTH Autism AND for Rett Syndrome

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 8,410,000 NTI shares and 350,000 options at the time of publishing this article. The Company has been engaged by NTI to share our commentary on the progress of our Investment in NTI over time.

Both trial results are in.

And both are a success.

(ie, the trials met their “primary endpoints” - proving the hypothesis that the treatments are effective)

After a long wait, this is what we were hoping to see.

There is still more data to come from the Rett Syndrome treatment trial in 2 to 4 weeks.

Today, our biotech Investment Neurotech International (ASX:NTI) announced that BOTH of its clinical trials for Autism Spectrum Disorder (ASD) and Rett Syndrome had met the trials’ primary endpoints.

Primary endpoints are the key metrics on which clinical trial success is judged - they show if a treatment WORKS.

By meeting the primary endpoint NTI has shown that its treatment for Autism and Rett Syndrome shows “statistically significant improvement” in symptoms for patients.

We think this opens the door to discussions with regulators about bringing the treatment to market, potentially an additional trial, and (we hope) ultimately, commercialisation.

AND it means NTI is now in a great position to advance its treatment for ASD and Rett Syndrome, and in doing so, help patients, carers and the broader health system.

That’s a big win.

We’ve got our breakdown of the results today, and what’s next for NTI...

The results were also good enough for NTI to quickly seal an in demand $10M capital raise at 10c/share from institutional investors.

(We bid $150k and got scaled back to $70k)

That means NTI now has the financial firepower to start another trial on Cerebral Palsy - another nasty condition.

And also talk to EU and US health authorities about Orphan Drug Designation for Rett Syndrome.

Both the Cerebral Palsy trial and Orphan Drug Designation shape as major additional wins.

The ball is well and truly rolling for NTI, can the company kick more goals?

We think so.

Here’s what we’re looking forward to most after today’s results:

- ASD - TGA regulatory advice is the next main thing, this will let NTI know if its treatment is suitable for the Australian market in the eyes of the regulator.

- Rett Syndrome - Orphan Drug Designation from the US FDA and EU EMA - both very valuable outcomes.

- Cerebral Palsy - start of a new trial, with a large market opportunity, another catalyst.

This isn’t a full list, there’s plenty more newsflow to come from NTI - this is discussed later in the note.

And at 12PM AEST today, a full discussion of the clinical trial results, presented by NTI’s Dr Thomas Duthy, can be viewed via the webinar link below (we’ll be attending):

Click here to register for the NTI results webinar

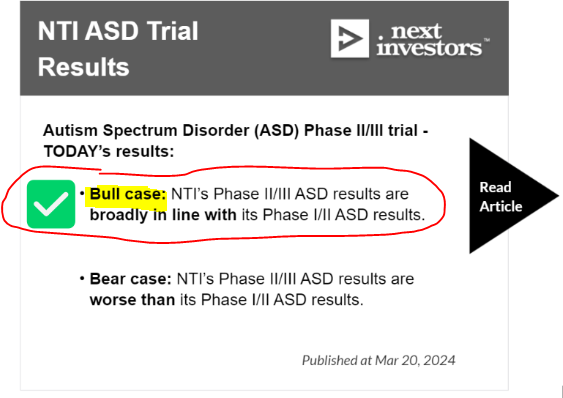

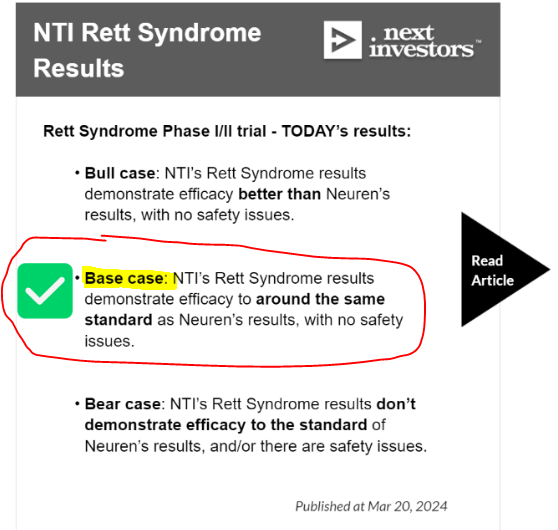

We think the ASD trial hit our BULL CASE and the Rett Syndrome trial hit our BASE case - which is still really good, and could even make NTI eligible for Orphan Drug Designation and (hopefully, eventually) FDA approval.

TODAY’s results:

(Click here to read our bull, bear and base case article)

(Click here to read our bull, bear and base case article)

Our NTI Big Bet

“NTI re-rates to a +$500M market cap by successfully advancing one or more of its clinical trial programs through to regulatory approval, partnership/licensing and/or is acquired by a large pharmaceutical company”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved - just some of which we list in our NTI Investment Memo. Success will require a significant amount of luck. There is no guarantee that our Big Bet will ever come true.

More on today’s NTI results...

Key takeaways:

- NTI’s ASD results were broadly in line with its previous Phase I/II ASD clinical trial results - which were (to us) outstanding.

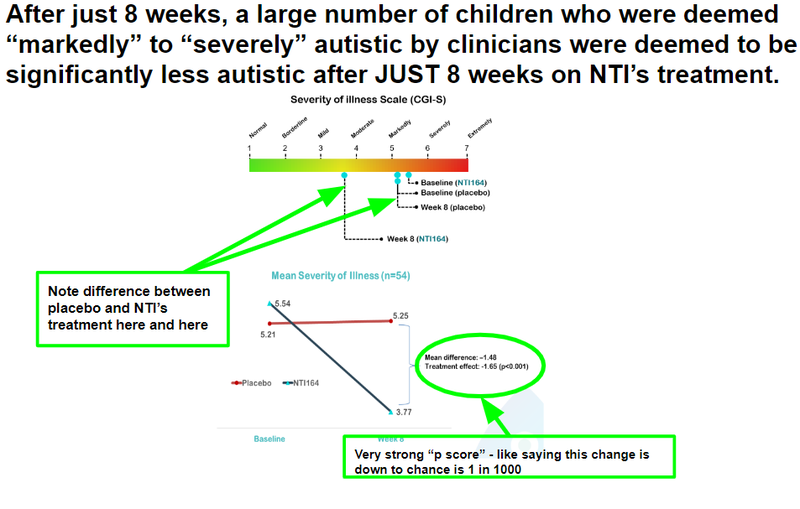

A large number of children who were deemed “markedly” to “severely” autistic by clinicians were deemed to be significantly less autistic after JUST 8 weeks on NTI’s treatment.

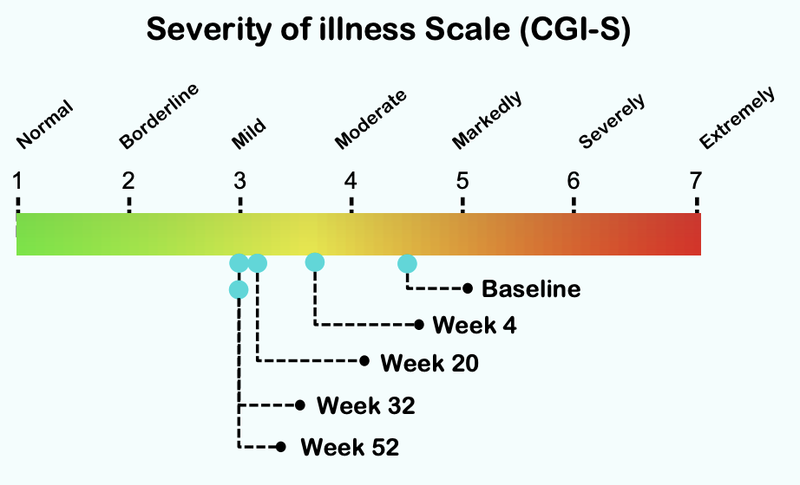

In the previous ASD Phase I/II trial, which was extended, improvement continued out to 52 weeks - so further results from the current Phase II/III, which has also been extended, could yield more positive data.

There are no FDA approved treatments for autism - and off-label treatments are used.

Market opportunity: An annual drug therapy market of at least ~US$2BN.

For a full breakdown of of how we think NTI’s treatment for ASD could help the NDIS (which has an expensive autism bill) read this note:

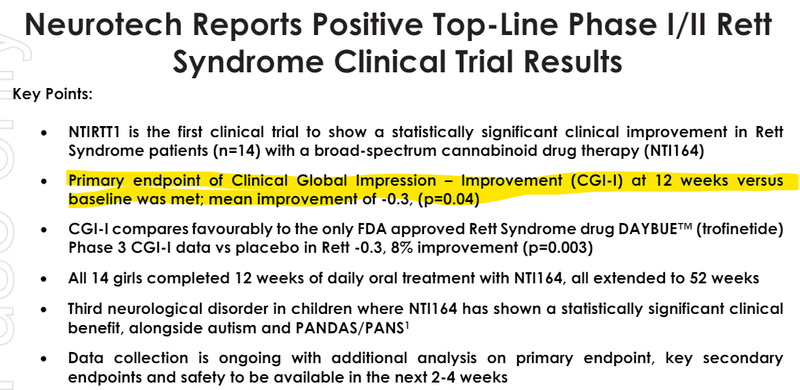

- NTI’s Rett Syndrome results demonstrated efficacy to around the same standard as Neuren’s results, with no safety issues.

The mean difference on the primary endpoint (CGI-I) was EXACTLY the same as Neuren Pharmaceuticals Phase 3 results (-.3) which got Neuren FDA approval and re-rated its share price more than 2,000%.

BUT with no serious safety issues - Neuren’s treatment has some considerable questions around its safety.

Market opportunity: An annual drug therapy market of ~US$2BN.

Granted, the “p score” on NTI’s results was not as good as Neuren’s “p score” BUT, whilst we are not professional statisticians, we think this is largely down to the cohort size (number of kids treated in the trial). We think the “p score” could come down in a subsequent NTI Phase III on Rett Syndrome with a larger cohort.

In other words, we think the Rett Syndrome results could form the basis for FDA approval if they are further proven out, given NTI’s similar efficacy to Neuren’s and NTI’s, so far established, better safety profile.

For a full breakdown of of how we think NTI’s treatment for Rett could potentially prove to be better than Neuren’s treatment read this note:

Now here’s a bit of a guide on how to read today’s results...

It starts with the premise that we all want safe and effective medicines and therapies.

Clinical trials determine efficacy and safety through endpoints.

An endpoint is “a targeted outcome of a clinical trial that is statistically analysed to help determine the efficacy and safety of the therapy being studied”. (Source)

There are both primary endpoints and secondary endpoints:

“Primary endpoint(s) are typically efficacy measures that address the main research question. Secondary endpoints are generally not sufficient to influence decision-making alone, but may support the claim of efficacy by demonstrating additional effects or by supporting a causal mechanism.” (Source)

NTI’s ASD Phase II/III trial results explained...

The primary endpoint on NTI’s Phase II/III is called Clinical Global Impression-Severity (CGI-S).

“CGI-Severity (CGI-S). The CGI-Severity (CGI-S) asks the clinician one question: “Considering your total clinical experience with this particular population, how mentally ill is the patient at this time?” which is rated on the following seven-point scale:

- 1 = normal, not at all ill;

- 2 = borderline mentally ill;

- 3 = mildly ill;

- 4 = moderately ill;

- 5 = markedly ill;

- 6 = severely ill;

- 7 = among the most extremely ill patients.

This rating is based upon observed and reported symptoms, behaviour, and function in the past seven days.” (Source)

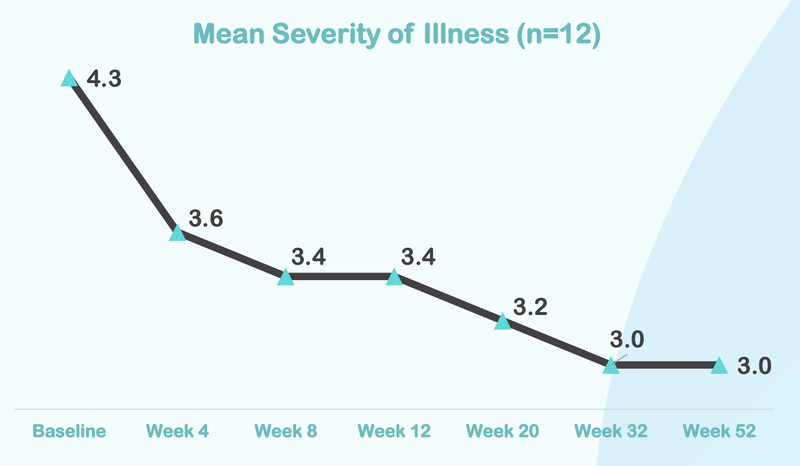

These were NTI’s results along CGI-S in its Phase II/III trial:

(Source)

And these were the results from NTI’s previous Phase I/II ASD trial that tested for both efficacy and safety...

It looks pretty much the same - which is great news.

From this chart you can see that the severity of illness for children with Autism moved from “Markedly” to “Mild”:

Here is how the treatment reduces over time, with significant improvement after just four weeks of taking the treatment:

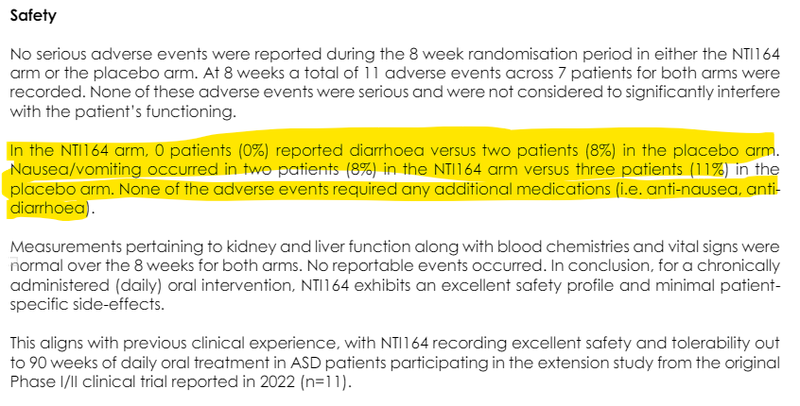

And again - in the Phase II/III trial the safety looks to be clearly excellent:

(Source)

Placebo actually showed worse side effects - which is more good news for NTI’s treatment.

Autism Spectrum Disorder (ASD) is estimated to affect around 1 in 100 children around the world, and in Australia, 35% of the ~610,000 National Disability Insurance Scheme (NDIS) participants have ASD, and 78% are under 18 years old.

If NTI’s treatment is proven safe and effective for ASD, we think it could become an important part of the overall care for ASD sufferers, ease the burden on both carers and government programs, and as a result, make NTI’s treatment commercially attractive.

We see NTI’s ASD trial results as potentially opening up a large Total Addressable Market (TAM) commercialisation opportunity in Australia - and (we hope) with the rest of the world, in particular the lucrative US healthcare market to follow subsequently.

NTI’s Rett Syndrome Phase I/II trial results explained...

In the case of the NTI’s Rett Syndrome results - we are most interested in the primary endpoint which is called Clinical Global Impression – Improvement (CGI-I).

CGI-I “provide[s] a brief, stand-alone assessment of the clinician's view of the patient's global functioning prior to and after initiating a study medication.” (Source)

Think of it as a standardised barometer of how a clinician views the effectiveness of NTI’s medication in improving the neuropsychiatric symptoms of Rett Syndrome.

As we said in our last NTI note:

“Now, if NTI can get a good CGI-I endpoint score - then we think NTI’s treatment could be well received in the market”.

Particularly considering, the current standard of care for Rett Syndrome is Neuren Pharmaceuticals' Daybue treatment - which helped Neuren re-rate more than 2,000%, despite a recent short report which questioned the safety of the treatment.

(Read our note on this short report).”

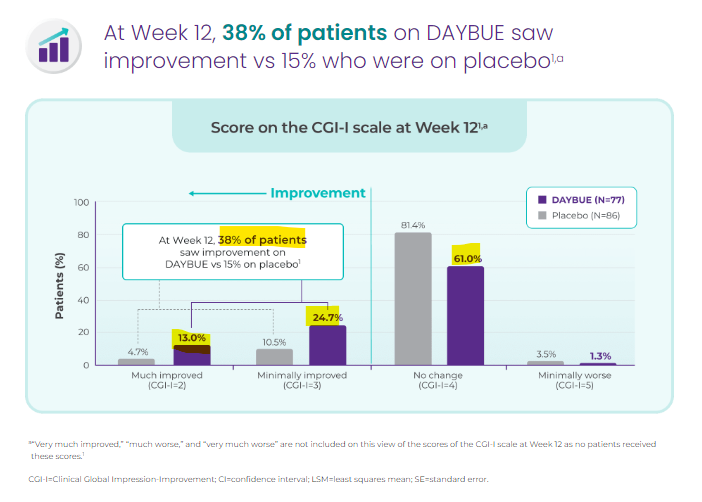

So what does a good CGI-I score look like for NTI?

We think the best reference point is Daybue’s metrics - which received FDA approval.

Daybue was the first and so far, only FDA approved treatment for Rett Syndrome.

Now looking at Daybue’s CGI-I scores:

(Source)

As we can see, 38% of patients saw improvement, and 61% of patients saw no change on the Daybue treatment from Neuren Pharmaceuticals.

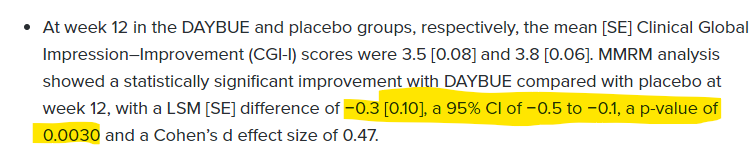

These were Neuren’s Phase 3 results:

(Source)

These are NTI’s CGI-I results for Rett Syndrome:

(Source)

We think the results are largely comparable - granted, the “p score” on NTI’s results was not as good as Neuren’s “p score” - and whilst we are not professional statisticians, we think this is largely down to the cohort size (number of kids treated in the trial). We think the “p score” could come down in a subsequent NTI Phase III on Rett Syndrome with a larger cohort.

In other words, we think the Rett Syndrome results could form the basis for FDA approval if they are further proven out, given NTI’s similar efficacy to Neuren’s and NTI’s, so far established, better safety profile.

Given Neuren’s FDA approval on these CGI-S scores, we feel like that is a relatively low bar for NTI to step over with its treatment.

We’ve already seen that NTI’s treatment is generally well tolerated in terms of safety across multiple trials for different disorders already, so we don’t think safety will be a major concern if a Phase 3 trial is pursued (noting that things can still go wrong).

As a reminder...

Rett Syndrome is a rare genetic neurological and developmental disorder that affects the way the brain develops in very young women.

Rett Syndrome symptoms are horrible and permanently life altering for both the patient and caregivers.

Children with Rett Syndrome can experience:

- delayed development milestones,

- loss of motor skills,

- seizures,

- intellectual disabilities,

- sleep disturbance,

- behavioural problems,

- social anxiety,

- poor coordination,

- and vision problems.

Sadly, right now there is no cure for Rett Syndrome.

And as a result, Rett Syndrome is considered an Orphan Disease considering there is only one FDA approved treatment that aims to reduce its impact and severity.

That FDA approved treatment belongs to ASX listed Neuren Pharmaceuticals - the drug is called ‘Daybue’.

In 2018 Neuren closed a licensing deal for Daybue with a NASDAQ listed company called Acadia Pharmaceuticals ($6.3BN market cap).

Between 2020 and 2023, FDA approvals and commercialisation took Neuren’s market cap from ~$100M to a peak of $3.3BN.

Neuren is currently capped at $2.5BN.

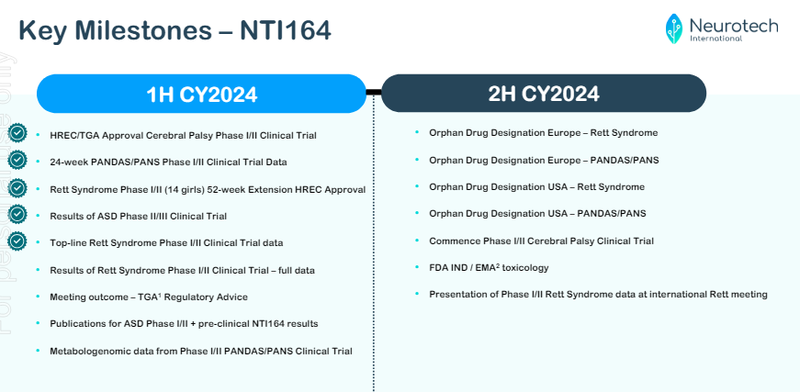

What’s next for NTI...

NTI has always been good at signalling clearly what newsflow is to come, and delivering that newsflow on time.

There’s a heap of newsflow to come too:

(Source)

Here’s our highlights of what’s next for NTI for the rest of year with our commentary:

Results of Rett Syndrome Phase I/II Clinical Trial - full data

This will include results from NTI’s secondary endpoints - and paint a better picture of its potential efficacy across these metrics.

Meeting outcome - TGA Regulatory Advice

Given the ASD results, we expect NTI will engage with the Therapeutic Goods Administration (TGA) in Australia to see if the TGA supports the treatment entering the market.

Metabologenomic data from Phase I/II PANDAS/PANS Clinical Trial

This is actually quite important - this is another measure of how well NTI’s treatment works for another rare paediatric disorder called PANDAS/PANS.

Results have already come back positive for this disorder in October of last year - this could show the method of action of NTI’s treatment, further strengthening its case for entry to market.

Read about PANDAS/PANS:

NTI’s clinical trial meets primary endpoints for neurological disease

Orphan Drug Designation Europe - Rett Syndrome

Orphan Drug Designations are very valuable and can fetch large sums of money - Neuren’s Orphan Drug Designation was worth roughly $100M. If the EU gives the all clear, this catalyst could re-rate NTI’s share price.

🎓Learn: Orphan Drugs Explained

Orphan Drug Designation Europe - PANDAS/PANS

Same applies for PANDAS/PANS

Orphan Drug Designation USA - Rett Syndrome

The US healthcare market is incredibly lucrative - US Orphan Drug Designation for Neuren played a major role in its 2000% re-rate.

Orphan Drug Designation USA - PANDAS/PANS

Same applies for PANDAS/PANS in the US

Completion of Patient Recruitment Phase I/II Cerebral Palsy

We expect NTI to start recruiting for this trial which could add another big string to NTI’s bow.

NTI already has Human Research Ethics Committee (HREC) approval and Clinical Trial Notification (CTN) scheme clearance by the Therapeutic Goods Administration (TGA) for this trial.

Cerebral Palsy is a group of permanent movement neurological disorders, appearing in early childhood.

It impacts muscle coordination and motor-neuron skills, but can often impact other body parts too. No two people experience CP in the same way.

Market opportunity: An annual drug therapy market of US$4.3BN.

Rare disorder - potential orphan drug designation could make NTI’s treatments lucrative.

At the moment there are only two FDA approved drugs available.

Commence Phase I/II Cerebral Palsy Trial

Starting the trial would open up another catalyst for NTI on results.

FDA IND/EMA toxicology

US FDA Investigational New Drug and European Medicines Agency toxicology reports will hopefully show that NTI’s treatment is safe in the human body - this can only strengthen NTI’s case for market entry.

Presentation of Phase I/II Rett Syndrome data at international Rett Syndrome conference

Neuren previously presented its results here - we’d like to see NTI do the same to build support for its treatment in the broader Rett Syndrome community.

Risks

The two key risks to our NTI Investment Thesis prior to today’s results were “Clinical trial risk” and “Funding/Dilution risk”.

With NTI’s two clinical trials meeting their primary endpoints, and a $10M raise tucked away we now see two different risks, which are - “Regulatory risk” and “Market risk”.

Regulatory risk:

We see the upcoming discussions with EU and US regulators about Orphan Drug Designation for PANDAS/PANS as key catalysts - regulators could decide that NTI’s drug does not qualify.

Orphan Drug Designations are very valuable and can be on-traded for cash or kept by the company.

If NTI doesn’t get these designations, then it could hurt the NTI share price.

Market risk:

Broader market sentiment for small pre-revenue biotechs could get worse and the sector as a whole trades lower, taking NTI’s share price with it. Alternatively, the entire market could sell down as well.

We note extremely heightened geopolitical tensions, and the potential for a wider conflict in the Middle East.

World events could drag the NTI share price lower, even if it does everything right.

Our NTI Investment Memo

In our NTI Investment Memo you’ll find:

- Key objectives for NTI

- Our long term NTI Big Bet

- Why we are Invested in NTI

- What the key risks to our Investment

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.