New Investment: Lithium in Canada with a side of US Rare Earths

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 9,740,545 MEG shares and 350,000 MEG options at the time of publishing this article. The Company has been engaged by MEG to share our commentary on the progress of our Investment in MEG over time.

Today we’ve added a new Portfolio Investment.

An early stage explorer that’s chasing two of our favourite commodities — lithium and rare earths — in North America.

Megado Minerals (ASX:MEG) has just acquired a lithium project in the same region of Canada as lithium market darling, the ~$1.7BN Patriot Battery Metals.

The vendor of the MEG assets also vended part of the Patriot assets into that company - part of the Corvette discovery, which led it from a $553M IPO in December 2022 to its current market cap of ~$1.7BN.

MEG’s on the ground exploration in Canada will be conducted by a related entity of the vendors - these folks were intimately involved in Patriot’s discovery, pre and post its IPO.

Post transaction, the vendors will hold ~ 18% of MEG shares, and a related entity will be conducting 3 years of exploration work for MEG.

So MEG is not just getting a prime piece of real estate it’s also got an on the ground exploration team incentivized for success.

MEG’s picked up a 130 km2 contiguous package of claims in the James Bay region of Canada.

This region is a fast emerging lithium hot spot, with not only Patriot but the $318M capped Winsome Resources also successfully making a lithium discovery.

While MEG isn’t expecting to drill in the James Bay until the end of 2023, we expect that the success of Patriot could generate some buzz and interest in MEG’s drilling campaign in the lead up to that program.

MEG’s ground is in the underexplored Aquilon Greenstone Belt. Greenstones are the type of rocks that are known to host valuable mineralisation — the same kind of rocks that delivered Patriot’s lithium discovery.

So MEG is in the same region as Patriot, and has ground with similar geology and a similar structural setting which is favourable for lithium discoveries.

The ingredients are there, but we won't know how much MEG’s ground is worth until it gets out there and starts drilling, and that is a little while off yet.

It’s very early days here.

Again, we are unlikely to see drilling here until later in 2023, but with a $11.2M market cap we like the upside MEG presents.

MEG has just received commitments for a $2.7M capital raise at $0.045 which we participated in. However, settlement won't be until late March — likely around the time the acquisition will be completed.

Of course, this is a micro cap stock so comes with significant risks.

There is an extremely low chance that MEG ever reaches a similar market cap to that of Patriot (~$1.7BN).

BUT we are Invested just in case it does... even a fraction of Patriot’s return on a successful lithium hit would be a great result for MEG from current levels.

Our Investment thesis also includes the significant attention on Patriot driving investor interest to MEG’s maiden drilling campaign.

Today, we will be launching our 2023 MEG Investment Memo, where you can find:

- Why we Invested in MEG

- Our long term bet - what we think the upside Investment case for MEG is

- The key objectives we want to see MEG achieve over the next 12 months

- The key risks to our Investment thesis

- Our Investment Plan

Read our MEG Investment memo below or click here to read it or book mark it on our website.

Why we Invested in MEG

- Right place, right time (critical minerals exposure in North America) - US is planning to spend US$2 trillion over the next 10 years in order to reshore supply chains of critical minerals. Lithium and rare earths are listed as critical minerals as part of the US critical minerals strategy.

- Canadian lithium project in the right neighbourhood - MEG’s ground sits along strike to major lithium discoveries made by Patriot Battery Metals (capped at ~$1.7BN), Winsome Resources (capped at $318M).

- Similar geology to larger market cap neighbour - MEG sits on top of the same type of rock structures that host Patriot Battery Metals’ Corvette discovery.

- Project has never been explored for lithium - MEG’s lithium project has never been explored for lithium with most of the historical exploration focused on gold. This is despite previous mapping identifying >1km long pegmatite outcrops on projects next to MEG’s.

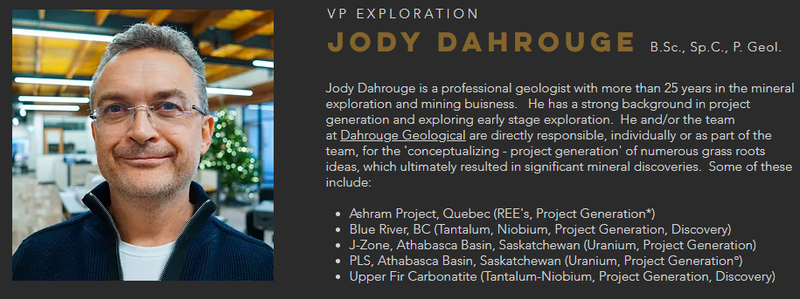

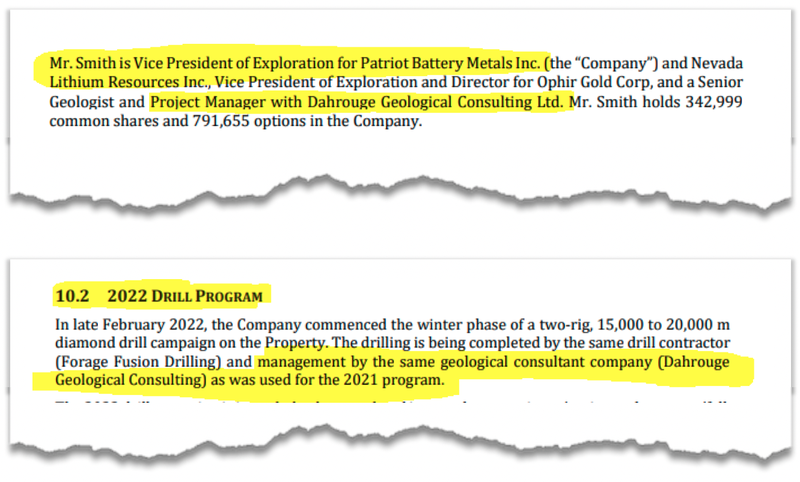

- Vendor of the MEG project was involved with Patriot Battery Metals, retained as a consultant - The vendors of the assets to MEG are from Dahrouge Resource Management, a related party of Dahrouge Geological Consulting (the company that did Patriot’s exploration work). Dahrouge Geological Consulting will be retained as consultants at MEG’s lithium project and have MEG shares which means they have skin in the game to deliver success for MEG.

- High grade rare earths in carbonatites - MEG’s US rare earths project has multiple carbonatite structures at surface across ~10km of strike. Rock chip sampling across the project has returned grades of up to 17.7% TREO (Total rare earths oxide). Carbonatites are the same type of rocks that hosts $7.6BN Lynas Rare Earths Mount Weld rare earths project.

- Low EV, leveraged to a discovery - MEG is currently trading with a market cap of $11.2M, has $3.5M in cash in the bank trading with a tiny Enterprise Value of $7.7M.

Our Big Bet:

“MEG returns 10x by making a North American critical minerals discovery significant enough to move into development studies, or attract a takeover offer”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is a lot of work to be done, many risks involved, and it will require a significant amount of luck. There is no guarantee that it will ever come true. Some of these risks we list in our MEG Investment Memo.

What we want to see MEG achieve:

Objective #1: Complete target generation works at Canadian lithium project

- We want to see MEG rank high priority drill targets.

- Ultimately we want to see the company identify spodumene bearing pegmatites and define high priority drill targets.

Milestones:

🔲 Geological mapping

🔲 Rock chip sampling

🔲 Define high priority drill targets.

Objective #2: Complete target generation works at US rare earths project

- We want to see MEG put together a list of high priority drill targets.

Milestones:

🔲 Geological mapping

🔲 Rock chip sampling

🔲 Geophysics

🔲 Define high priority drill targets.

Objective #3: Drill program at Canadian lithium project

- We want to see MEG drill test the high priority targets identified in Objective #1.

Milestones:

🔲 Drilling permitting

🔲 Drilling commencement

🔲 Drilling results

Objective #4: Drill program at US rare earths project

- We want to see MEG drill test the high priority targets identified in Objective #2.

Milestones:

🔲 Drilling permitting

🔲 Drilling commencement

🔲 Drilling results

What are the risks?

Exploration risk - the projects that MEG is working on are early stage projects. As with any exploration company, there is always a chance that after drill testing its targets, MEG returns no mineralisation or uneconomic lithium grades and the project is considered “stranded”. The same risk applies to the drill targets that MEG defines at its rare earths project.

Market risk (macro) - broader market conditions could change for the worse. This could mean that small cap exploration stocks like MEG suffer from a “risk off” market move.

Commodity price risk - lithium and rare earths prices could fall, or enter a prolonged downturn. In turn, hurting the economics of any future project that could come from MEG’s drill programs. Even if MEG makes a discovery there is no guarantee that lithium and rare earths maintain their appeal in the market.

Funding risk - as a junior exploration company, MEG will need to seek additional capital to advance the company’s projects. Access to this capital could be impacted by any of the three risks above.

Delay risk - it is possible that there are delays getting permits or weather preventing drilling from proceeding. Any delays with material newsflow can impact a small cap stock like MEG as investors may lose interest as a result of the delays.

What is our investment plan?

After investing in an earlier round as part of the rare earths acquisition, our Initial Entry Price for MEG is $0.039 cents.

As with all our new exploration investments, if the share price runs in the lead up to drilling or on a great drill result (by more than 300%), we will likely de-risk by Top Slicing 20% of our Total Position, in the hope to achieve Free Carry into the remaining drill campaigns.

This is our standard plan across all early stage exploration Investments.

The rest of the Investment plan depends on the outcomes of the company’s drill campaign and will be updated accordingly, and be governed by the 2 to 3 year holding periods as defined in our trading and hold policy disclosure.

Two months ago, a lithium company called Patriot Battery Metals IPO’ed and listed in both Canada and Australia with a market valuation of ~$550M.

Now with a market cap of ~A$1.7BN, the success of the Patriot Battery Metals IPO has demonstrated the power of having a great project in the right place and the right time.

It’s clearly “go time” for North American critical minerals projects, and we’ve been closely tracking companies that can give us the right exposure to this theme.

The North American critical minerals rush was ignited by the US$400 billion “Inflation Reduction Act” (IRA), which was a measure that the US government signed into law in August of last year.

For context, the US has now signed into law US$2 trillion (including the IRA) in policies aimed at reshoring its critical minerals supply chains over the next 10 years.

For these reasons, we are intentionally targeting North American critical minerals for our Portfolio. Here’s our take from a few weeks ago on the thematic.

Our MEG Investment in particular is designed to capture the macro tailwinds that the IRA created as North America focuses its attention on re-shoring its critical minerals supply chain.

Sidenote: We had great success with this thematic in Europe with our Investment in lithium explorer Vulcan Energy Resources - its share price went from 20c to a peak of ~$16 per share - a return of almost ~8,000% at its peak (we are not saying MEG will do this too, but even if it delivers a small portion of these returns, it will be an excellent result).

MEG is an early stage explorer going after BOTH lithium and rare earths discoveries INSIDE the US and Canada.

Here’s the quick rundown on each project:

North American critical minerals project #1: Canada lithium

MEG is acquiring ~130km2 of ground in the James Bay region of Canada which is fast becoming one of the most significant hot spots for lithium exploration in North America.

James Bay is home to Patriot Battery Metals (capped at ~1.7BN)) and Winsome Resources (capped at $318M).

Given lithium’s appeal - we suspect this will be the project the market is most interested in.

However, it won't be the next project they drill. For that we look south to Idaho, USA, and in particular, for rare earths...

North American critical minerals project #2: USA Rare Earths

Located in Idaho, USA, MEG has 42km^2 of ground which has multiple carbonatite structures at surface across ~10km of strike.

Rock chip sampling across the project has returned grades of up to 17.7% TREO (Total Rare Earths Oxide).

Carbonatites are the same type of rocks that hosts the $7.4BN Lynas Rare Earths Mount Weld rare earths project.

The USA currently has only one active rare earths mine.

It’s not happy China has most of this market wrapped up. The USA would desperately like to see some local rare earths discoveries so it can build up its own supply chain and remove reliance on China.

We are Invested in MEG to see it try and make a rare earths/lithium discovery INSIDE North America.

MEG will hold ~130km2 of ground with similar geological features to ~$1.7BN Patriot Battery Metals.

Patriot is capped at ~$1.7BN primarily because it is trading on a post-discovery valuation.

MEG on the other hand is capped at $11.2M, has $3.5M in cash once today’s capital raise has settled - and therefore trades with an enterprise value of just $7.7M.

MEG’s other project is a rare earths project where the company is looking to make a carbonatite hosted rare earths discovery in Idaho, USA.

Carbonatites are the same type of rocks that host Lynas Rare Earths already producing Mount Weld rare earths project.

Mount Weld is considered one of the world's highest grade rare earths mines with grades of up to ~5.4%.

It’s early days, but MEG’s project has already confirmed rock chip samples grading up to 17.7%. We will be watching for MEG to drill its highest priority targets and (we hope) make a discovery.

For now, across both projects, the company is focused on defining high priority drill targets.

Next, we want to see the company get drill rigs on the ground and have a shot at a discovery at both of its projects.

Drilling on the rare earths project is expected to happen around mid 2023, with lithium drilling expected around the end of the year.

More on the vendor of MEG’s Canada lithium project:

The vendors of the assets to MEG are from Dahrouge Resource Management, which is a related party of Dahrouge Geological Consulting (the company that did Patriot’s exploration work).

Post acquisition Dahrouge Resource Management will hold ~18% of MEG shares. We like this as it aligns the exploration team to other MEG shareholders.

Jody and Simon Dahrouge are the VP, Exploration and Exploration Geologist respectively at Dahrouge Resource Management.

You can see a nice profile of Jody Dahrouge’s work below:

And Simon as well:

Dahrouge Geological Consulting managed the exploration program for Patriot Battery Metals.

We like that the people, and MEG shareholders, who are intimately familiar with the project’s geology are being retained as consultants for 3 years - we imagine MEG will be using him to full effect to maximise the potential of the geology MEG is working with.

For more on the deal structure, keep reading.

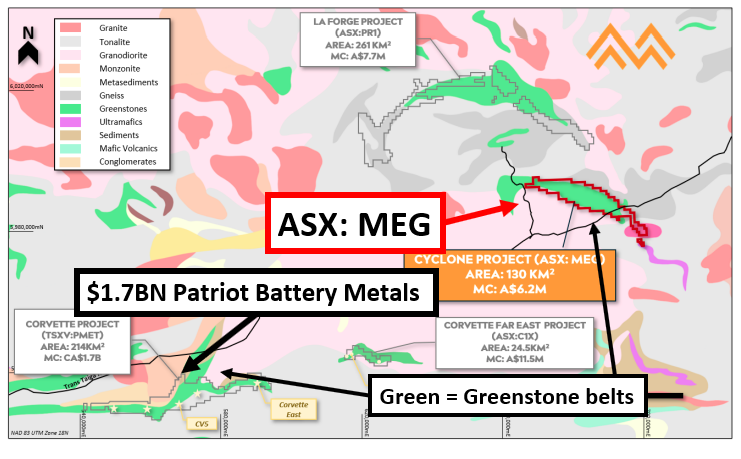

More on MEG’s geology - how does it compare to ~$1.7BN Patriot?

Remembering that MEG is capped at just $11.2M - MEG’s project shares geological and structural similarities with Patriot’s ~$1.7BN discovery.

Of course MEG’s project is at a far earlier stage (see risks section) and this needs to be taken into account.

As we see it, the key similarity is that the two projects sit right next to the same granite on greenstone rocks.

This type of granite/greenstone connection is typical of some of the largest discoveries made across the world.

The image below shows that connection with the Greenstone belts (Green) and Granites (Pink).

Typically large hard rock lithium discoveries are hosted in pegmatite structures that sit on top of this type of geology.

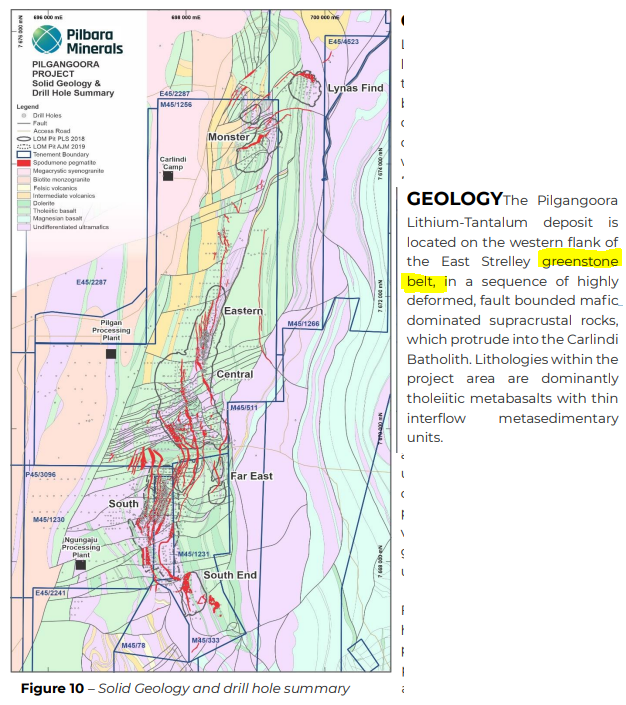

For some context, $14BN Pilbara Minerals Pilgangoora was discovered on top of a greenstone belt.

Interestingly, ground next door to MEG has already been mapped in the past and has confirmed pegmatite structures measuring >1km in length.

Most importantly though, MEG’s ground has never been explored for lithium, with all of the historic exploration over its project focused on gold.

MEG is acquiring the project at a time when the US government is desperate to secure local supplies of minerals like lithium which it lists as a “critical mineral” as part of its critical minerals strategy documents.

Lithium is a market almost exclusively controlled by China which has ~80% of the world's lithium hydroxide processing capacity.

Recognising that the only way to build local supply chains is to provide incentives to private industry, the US government recently gave ASX listed Ioneer Resources a US$700m conditional loan commitment for its US-based lithium project.

Should MEG make a discovery, we think the potential upside on offer means the company’s project has the potential to deliver the 1,000%+ returns we target when we Invest in micro cap companies (but we also keep in mind the risks which we list in our MEG Investment memo).

So what is MEG paying for the project?

- CAD$250k cash.

- 45 million MEG shares at 4.5c per share with the following escrow conditions:

- 4.5 million with no escrow.

- 20.25 million with a 6-month escrow.

- 20.25 million with a 12-month escrow.

As well as this MEG will issue the vendors 7 million options exercisable at 10c per share with a 3-year expiry and a 2% net smelter royalty for the project.

The shares are being issued to Dahrouge Geological Consulting - the same group that was involved in the discovery of Patriot Battery Metals’ Corvette project.

Below are excerpts from Patriot’s listing prospectus to the ASX where the company details Dahrouge’s involvement.

The same group will also be doing all of MEG’s exploration for at least the next 36 months.

With the group owning ~18% of MEG (45 million MEG shares) we think they are well aligned to try and deliver the company a successful discovery.

We think MEG has managed to acquire a relatively low cost exposure to a project that has serious company making potential.

Of course, all of this is conditional on MEG successfully making a discovery.

Post acquisition and capital raise MEG will have ~248 million shares giving the company a market cap (at 4.5c per share) of $11.2M.

MEG should have ~$3.5M in cash, trading at a tiny enterprise value of just $7.7M (based on the current share price).

This acquisition and capital raise still needs shareholder approval, and we expect the money to be in MEG’s bank account around late March.

For the next 6-9 months, MEG will be focused on defining high priority drill targets that will eventually be followed up with a drill program.

Our MEG Progress Tracker

We’ve been releasing “Progress Tracker” slide decks for our Portfolio companies.

Below is the MEG Progress Tracker document. We will use this internally to keep up to tabs on the company's progress. It shows how the project was brought into MEG and the progress made up to today, along with what we want to see the company achieve next.

Click here to check out our MEG Progress Tracker

If you want to follow the progress of our Investment in MEG over the next 3 years make sure you are subscribed to our Catalyst Hunter mailing list and read our weekend newsletter.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.