$24M capped LNR getting closer to drilling near its much bigger neighbours

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 19,823,582 LNR shares at the time of publishing this article. The Company has been engaged by LNR to share our commentary on the progress of our Investment in LNR over time.

Finally.

We have been covering Lanthanein Resources (ASX:LNR) since February 2022, waiting for its rare earths exploration project to be drilled, and it looks like we are almost there.

Today LNR announced that heritage surveys have begun, the precursor to the maiden drilling program at its rare earth elements project.

Rare earth elements, in particular the ones that LNR are exploring for, are important inputs for permanent magnets found in both electric vehicles and wind turbines.

As the world looks to ramp up its electrification and renewable energy capacity - rare earths are now strategic minerals.

That’s where LNR comes in.

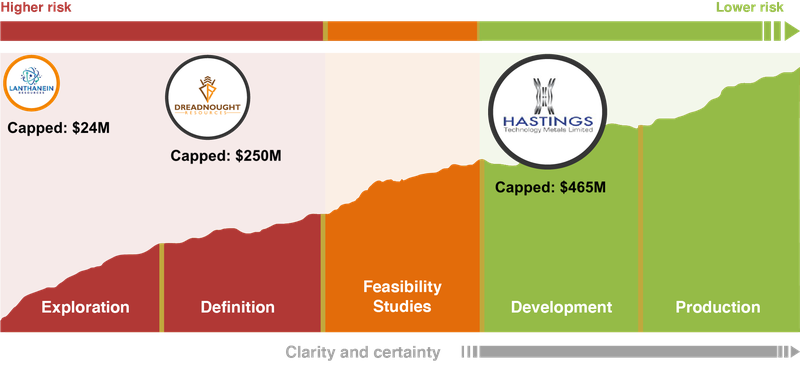

$24M capped LNR is exploring for rare earths in what is emerging as a highly valuable rare earths province in WA, nestled near two much bigger rare earths stocks:

- Dreadnought, capped at ~$250M

- Hastings Technology Metals, capped at ~$465M

Hastings’ rare earths project is currently being progressed into production and Dreadnought has made a rare earths discovery and is continuing to define its scope.

While LNR’s peers are more advanced, we are hoping that LNR can close the gap by making a new rare earths discovery with its first drilling program planned for early September.

Working in LNR’s favour ahead of drilling are:

- Rock chips grading as high as 8.01% - These were from outcropping ironstones which may mean there is more underground.

- Ironstones outcropping at surface - The same style of geology where Hastings made its discovery and Dreadnought recently drilled out rare earths.

- Geophysics targets - Pinpointing 12 different high priority drill targets.

- Drilling within close proximity of larger capped peers - The maiden drilling program is bordering Hastings’ Yangibana project and is <40km away from Dreadnought’s recent discovery.

Most importantly, LNR’s ground has never been drilled for rare earths before.

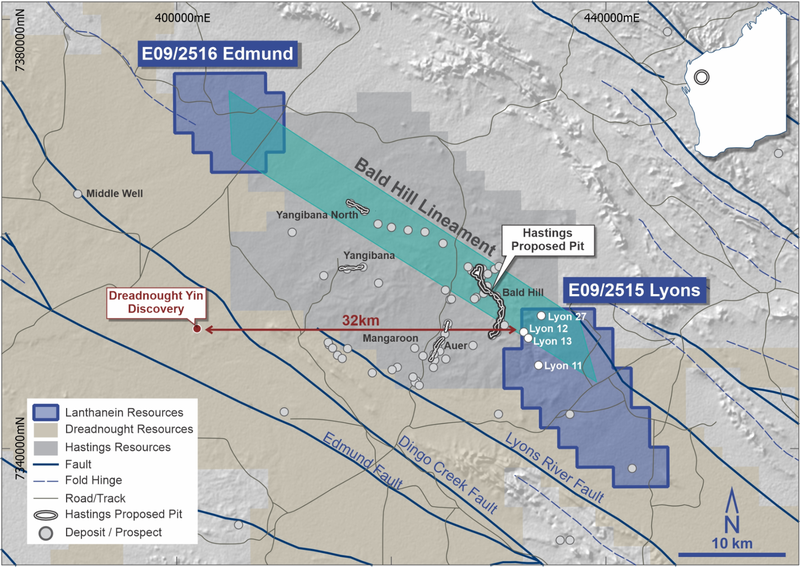

Dreadnought Resources (now capped at ~$250M), whose tenements lie immediately to the south of LNR’s prospects, moved from ~4 cents at the end of June to a recent high of 8.7 cents.

What triggered this was the company's high grade assay results from the first drill line at the Yin rare earth ironstones.

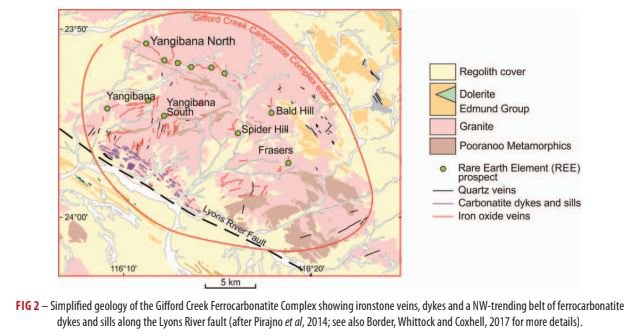

LNR is working with the same style of ground to Dreadnought’s Yin discovery - ironstone outcroppings, 32kms to the east:

LNR’s other neighbour, Hastings, has also recently reported solid extensional and in-filling drill results, ~2.5 kms to the west of LNR’s Lyons prospect.

Having looked at both Dreadnought’s drilling results and Hastings’ most recent drilling results we’ve outlined the following cases for LNR’s maiden drilling campaign:

Bull case: Significant mineralisation is found (approaching Dreadnought results, ~10-20m at 2-3% TREO)

Base case: Enough mineralisation is found to warrant follow up drilling (similar hits to nearby Hastings - ~5-10m at ~1-2% TREO).

Bear case: No mineralisation is found

Dreadnaught and Hastings are both capped at many multiples of LNR, so we think there could be room for significant value uplift for LNR should the maiden drill campaign go well.

After recently completing a $1.75M placement at 1.4c (which we participated in) and with $4M in cash in the bank (at 30 June 2022), we expect LNR to have ~$7.75M in cash/financial assets once their PNG gold project is sold.

LNR is currently trading with a market cap of $24M (after the placement shares are issued) meaning the company trades with an enterprise value (EV) of ~$16.25M, with what we view as plenty of room for upside.

Now for the drill bit to do the talking.

Background to LNR's drilling campaign

With the first green shoots of positive sentiment creeping back into the market, LNR’s major catalyst is just over the horizon.

The company has done a body of work ahead of drilling its Gascoyne rare earths project progressing towards Objective #2 from our LNR Investment Memo:

We think LNR has a lot going for it at the moment - rare earths companies on the ASX have been able to secure capital in difficult market conditions on the back of support from both the US and Australian governments.

Dreadnought raised $12M after some very good drilling results while the much larger Hastings Technology Metals secured a $140M loan facility from the Northern Australia Infrastructure Facility (NAIF) in February.

Further afield in the Northern Territory, Arafura Resources raised $41.5M this month in a placement to accelerate the company’s Nolans rare earths project.

This came after signing a non-binding offtake with South Korean carmaker Hyundai for their NdPr oxide product from 2025.

Nd and Pr are the two rare earth elements we are primarily looking for LNR to find, as these are found in the permanent magnets that go into making EVs and wind turbines.

In other words, if these two elements are found on LNR’s tenements in abundance, we think it would make LNR a viable home for capital seeking upside from the energy transition.

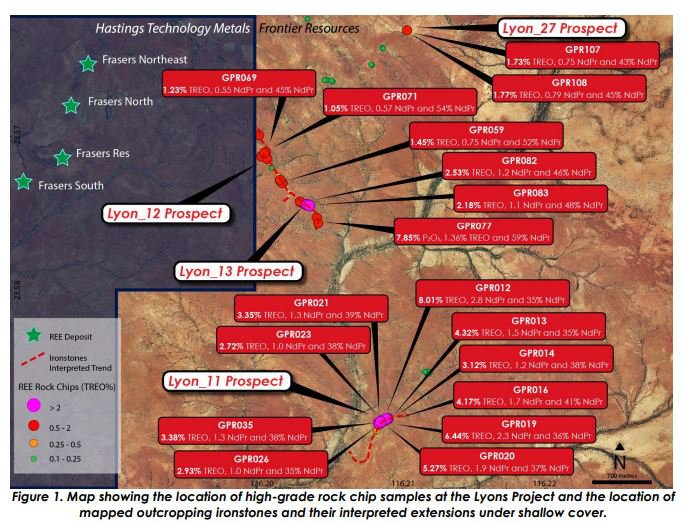

Again, LNR has already proven they have both Neodymium (Nd) and Praseodymium (Pr) in an extensive rock chip campaign that yielded a peak total rare earths oxide (TREO) result of 8.01%.

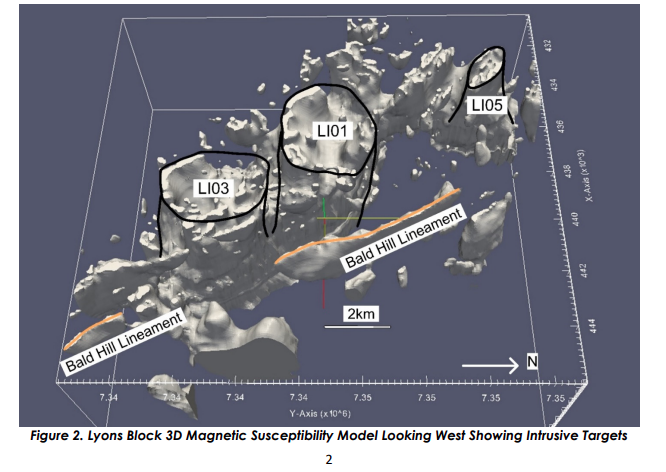

This was followed up by a geophysics survey which revealed three targets which are between 2-4km in diameter and go up to 2km deep.

With good rock chips in hand, three big geophysics targets, market sentiment towards rare earths remaining buoyant, a chunk of cash and significant government support, we are looking forward to LRN’s upcoming drilling campaign.

More on LNR’s upcoming drill campaign

We’re of the view that nothing has changed with regards to the prospectivity of LNR’s rare earths project since we first Initiated Coverage - if anything it’s improved as the company hones in on the best drill targets.

After a successful rock chip sampling program which returned a a peak total rare earths oxide (TREO) result of 8.01%, LNR has correlated the locations of these high grade ironstone rock chips:

With these three geophysics targets:

LNR believes these represent “larger tonnage style [rare earth element] REE targets that extend to over 2km depth”.

The 3D modelling LNR has put together include at least three different occurrences, varying in size as follows:

- Intrusive target LI01: 4.3km in diameter at surface, extending ~1km at depth.

- Intrusive target LI03: Circular ~2.8km diameter from a depth greater >2km.

- Intrusive target LI05: 2km x 1.3km structure with the source at ~2km depth.

LNR likens these targets to the circular carbonatite structure that gave rise to Australia’s largest rare earth mine, the Mount Weld Project.

Mount Weld is owned by Lynas Rare Earths - capped at ~$8.7B.

The Mount Weld Project is well defined by similar geophysical works that describe a “vertical cylindrical body, 3 to 4 km in diameter”.

Guiding LNR’s project is a highly respected geology academic and independent consultant called Franco Pirajno (bio from recent LNR announcement):

“Franco Pirajno is a highly cited researcher with considerable experience in the fields of tectonics, ore deposit geology and mineral exploration having worked extensively in Western Australia with published papers on both the Mt Weld and Gifford Creek REE Carbonatites. He is currently adjunct Professor at the Centre for Exploration Targeting (University of Western Australia).”

Pirajno literally wrote the book (or chapter) on Mount Weld and carbonatite structures.

In a chapter called “Mount Weld and Gifford Creek rare earth element carbonatites” that appeared in a book, Australian Ore Deposits, Piranjo and three other academics discussed the very same ground that LNR is working on:

We think it helps that LNR is working with Pirajno at their Gascoyne rare earths project and we note that Piranjo has approved the drill sites that LNR will test after reviewing the available data from LNR’s target generation works so far.

Which brings us to what LNR’s neighbours are up to.

LNR’s Gascoyne neighbours - peer comparison

So with LNR’s drilling program right around the corner, how does it stack up against its much larger capped neighbours?

The two neighbours in question are:

- Dreadnought Resources, capped at $250M

- Hastings Technology Metals, capped at $465M

First, Dreadnought.

Up until early June Dreadnought had a package of tenements to the West of Hastings’ project that held six ironstone outcroppings over a 10km x 5km area.

Importantly, Dreadnought at the time had rock chips taken from those outcrop’s grading as high as ~39.7% total rare earths oxide (TREO).

Similar to LNR, Dreadnought also had various different carbonatite structures over its project area with two of the six carbonatites confirmed as REE bearing (rock chips taken were grading up to 2.52% TREO).

At the time, Dreadnought traded with a share price of ~3.8c per share.

Everything changed for Dreadnought when, in mid June, the company hit a 33m intercept with a 2.25% rare earths grade basically from surface.

Dreadnought then followed that up in July confirming ~87% of its drilling had intercepted REE over ~3km of strike and that it had started infill resource drilling.

These are the most recent Dreadnought results that added fuel to its re-rate and precipitated a capital raise:

These results were very, very good for rare earth hits in the region which is why we’ve calibrated our bull case for LNR's drilling as follows:

Bull case: Significant mineralisation is found (approaching Dreadnought results, ~10-20m at 2-3% TREO)

Since then, the market has re-rated Dreadnought from ~3.8c per share to a recent high of ~8.7c per share, adding ~$142M to Dreadnoughts market cap at its peak.

This move alone is almost 6x LNR’s current market cap.

How does LNR compare?

- LNR has the same outcropping ironstones with rock chips grading as high as 8.01%.

- LNR also has a larger carbonatite structure modelled

The only difference is LNR is yet to drill its project but with the news today, LNR is set to drill in early September.

Second is Hastings Technology Metals.

The bigger and far more advanced, Hastings has a 27.4mt JORC resource with a TREO grade of ~0.94%, as well as an ore reserve of ~17.42mt @0.95%.

More importantly though, before the Yangibana discovery was made in 2014, in almost identical fashion to LNR and Dreadnought, Hastings ground was full of ironstone outcroppings where rock chips were returning grades as high as ~26% TREO.

Hastings had some historical drilling data on hand at the time and after drilling these areas then went onto make its Yangibana discovery later that year in July 2014.

Hastings' discovery came off the back of intercepts measuring between 4m-8m with TREO grades up to 3.44%.

Several years later the company has secured $140M in loan funding from the Northern Australia Infrastructure Facility (NAIF) and is progressing its project towards development.

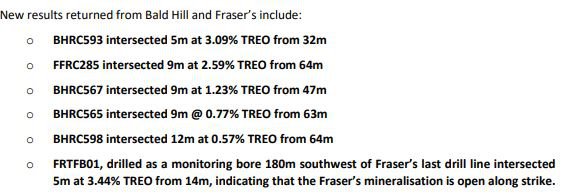

Meanwhile, Hastings’ most recent drilling at the Fraser’s and Bald Hill prospects just 2.5 kms away from LNR holds yielded the following results:

Given these results, we’ve calibrated our base case as follows:

Base case: Enough mineralisation is found to warrant follow up drilling (similar hits to nearby Hastings - ~5-10m at ~1-2% TREO)

Hastings currently trades with a market cap of $465M

This is almost 20x higher than LNR’s current market cap.

LNR currently trades with a market cap of $24M and will also be holding ~$7.75m in cash/financial assets (after the recent placement and gold project sale).

This means LNR currently trades with an enterprise value of just ~$16.25M at current prices, leading up to a potentially company making maiden drilling program.

Of course, despite the fact that we think LNR has a good chance of finding rare earths mineralisation in the drilling campaign, there’s also a chance that they find nothing.

For this reason, our bear case is that no mineralisation is found - part of exploration risk in our risks section from our LNR Investment Memo.

Risks

There are some material risks that we have highlighted in our Investment Memo for LNR:

Exploration Risks

When investing in early stage exploration, there is a chance that the company does not find anything - this would mean that our “Bear” case for the exploration program materialises.

Commodity Pricing

Commodity prices for rare earths, in particular the ones that LNR are looking for, remain strong.

However, sentiment can turn quickly, and LNR’s ability to develop a mine from any economic discovery made is dependent on these commodity prices.

Funding Risk

After recently completing a $1.75M placement and with $4M in cash in the bank at 30 June 2022, we expect LNR to have ~$7.75M in cash/financial assets once their PNG gold project is sold.

This materially de-risks the “Funding Risk” for LNR and provides the company with enough cash for the upcoming drilling program.

Delay Risk

There are a number of activities that take place on the path to drilling, and on this path are the heritage surveys which LRN just commenced.

Unfortunately for LNR this delay risk materialised (as it does with many small cap explorers) and heritage surveys were delayed a number of months.

Heritage surveys are an important part of the exploration program, where a qualified person will survey the land for Indigenous artefacts and / or the historical importance of the site.

As LNR outlined in a June announcement, a Covid case impacted their ability to complete the heritage surveys in a timely manner.

What’s next for LNR

Once the heritage survey is complete, we expect siteworks to begin with a drilling contractor already secured ahead of the early September commencement of the drilling program.

We’re also pleased to hear today that an additional Program of Works (PoW) application was lodged to allow for extended an extended drilling campaign, should early progress be made.

Our LNR Investment Memo

Below is our 2022 Investment Memo for LNR where you can find a short, high level summary of our reasons for investing.

The ultimate purpose of the Investment Memo is to track the progress of LNR throughout 2022 using the objectives set in the memo as our benchmark.

In our LNR Investment Memo you’ll find:

- Key objectives for LNR in 2022

- Why we continue to hold LNR

- What the key risks to our investment thesis are

- Our investment plan

Disclosure: S3 Consortium Pty Ltd (the Company) and Associated Entities own 19,823,582 LNR shares at the time of publishing this article. The Company has been engaged by LNR to share our commentary on the progress of our Investment in LNR over time.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.