ASX Stock Delivers One of the Highest Grade Copper JORC Resources in Australia: More to Come

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

Castillo Copper Limited (ASX:CCZ) is playing Dr Frankenstein and could be about to bring the dead back to life... in a big way.

The Cangai Copper Mine, part of the Jacakderry Southwest Copper Cobalt Project in NSW, has been the subject of intense exploration since the early 1900s, but was abandoned due to market forces and Rio Tinto’s takeover of Conzinc Riotinto of Australia (CRA).

Now CCZ has reopened the mine and is looking to resurrect it.

Today CCZ went a long way to doing so after announcing its first Copper-Cobalt-Zinc JORC compliant Inferred Resource; an exceptional high-grade Resource which has exceeded expectations with [email protected]% Cu implying c.108,000 tonnes of contained copper.

The result confirms that CCZ has one of the highest grade copper deposits in Australia.

This is intended to be the first JORC compliant copper-cobalt-zinc Resource of many for CCZ, with another due in just a week’s time at its Broken Hill zinc-silver project.

However, this remains a speculative investment and investors should seek professional financial advice if considering this stock for their portfolio.

Given its hold on legacy data from historical mining, including the in-depth analysis conducted by CRA, CCZ is able to fast track its Resources, with the company looking to prove up three JORC Resources across all its projects in quick succession.

Following that, in a move that will speak to the cost-effectiveness of its business strategy, CCZ then plans to use third party processors to fast track end-product sales to market via the London Metals Exchange to expedite cash flow.

The company’s focus right now, however, is on its Jackaderry Project and in particular the Cangai JORC Resource, which is set to increase substantially with incremental historic assay results and inaugural drilling campaign to begin in the coming weeks .

The project is supported by strong legacy data, most recently delivered by CRA before the Rio Tinto takeover.

Cangai is defined by the presence of very rare supergene ore, which implies the presence of an enriched copper resource. The Supergene zone is the richest part of the ore deposit and is close to surface.

Mine records show Cangai has up to 35% copper, occurring close to surface. The presence of supergene ore means it should be suitable for direct shipping ore (DSO) that can be easily transported to Newcastle port via excellent infrastructure already in place.

Importantly for CCZ, its supergene is similar to that held by the $904 million capped Sandfire Resources (ASX:SFR), the second largest ASX-listed copper-gold producer. Sandfire’s DeGrussa operations have had six years of consistent, safe and profitable production and is looking at 63-66kt of production in FY 2018.

CCZ is hoping its supergene ore at Cangai can deliver similar results.

All up, CCZ’s current Australian assets comprise of eleven highly prospective copper-cobalt-zinc project areas in NSW and Queensland. These areas include:

- Jackaderry North and Jackaderry South cobalt projects, prospective for copper-cobalt;

- Peak Hill and Total Mineral projects, 20km from Broken Hill, prospective for copper-cobalt-zinc; and

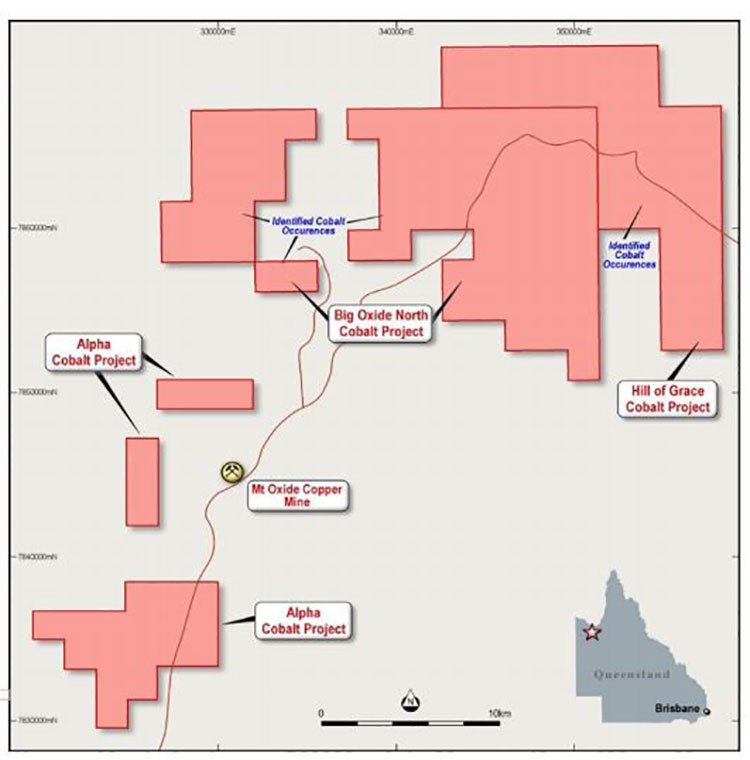

- Big Oxide North and Hill of Grace cobalt projects in Queensland, prospective for copper-cobalt.

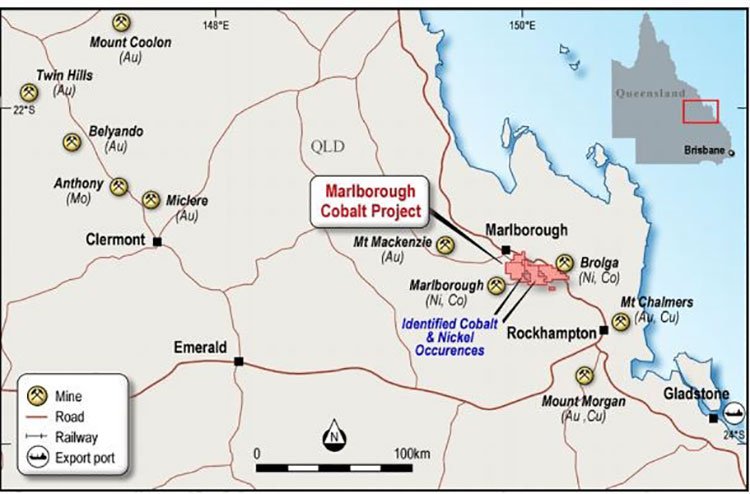

- Marlborough projects in Queensland, prospective for cobalt-nickel.

The Cangai catalyst: Copper-cobalt-zinc Resource defined

With CCZ intent on delivering three JORC Resources in quick succession, its focus has been on Cangai, where it has just delivered its first Resource – potentially one of the highest-grade copper Resources in Australia

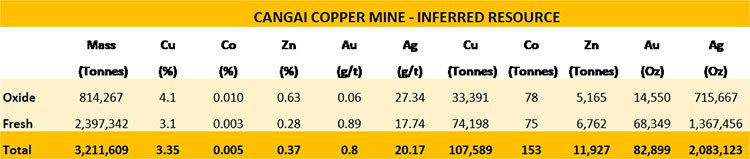

Today’s announcement highlights a high-grade maiden JORC Inferred Resource for Cangai Copper Mine in unmined working sections of 3.2Mt @ 3.35% Cu which implies circa 108,000 tonnes of contained copper.

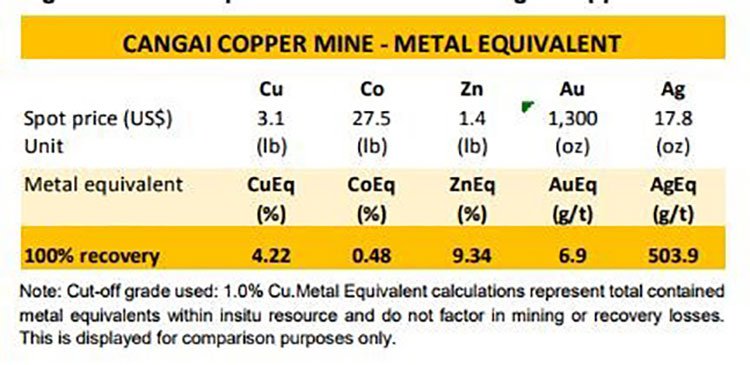

On a metal equivalent basis the key base metal results are: CuEq – 4.2%, ZnEq – 9.3% and CoEq – 0.5%, AuEq – 6.9g/t, and AgEq – 503.9g/t.

As this only accounts for a small part of CCZ’s Jackaderry Project, the Board is optimistic incremental desktop work and a maiden drilling program will underpin further exploration and Mineral Resource size upside moving forward.

We can’t highlight enough that the overall results achieved from analysing and 3D modelling legacy data for the Cangai Mine are exceptional and arguably one of the highest grades in Australia.

Here’s a look at the numbers:

The result delivers CCZ significant exploration upside and the potential to increase the Mineral Resource size within the Cangai Mine and holistically across the Jackaderry Project.

How did CCZ get to this point? A little history

A preliminary report from geology consultant ROM Resources showed mineralisation for copper-zinc-cobalt-gold-silver in unmined areas of Cangai that was open in all directions.

Notably, the historic Cangai Copper Cobalt Mine (within Jackaderry South prospect) confirmed deposits of supergene ore with up to 35% copper.

We will get to how important supergene is shortly, but first let’s take a broader look at Cangai to see how the JORC was delivered.

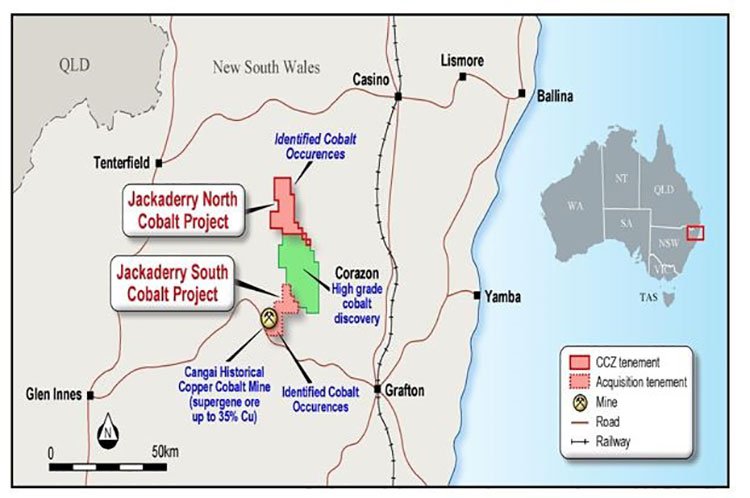

Here’s the lay of the land.

You can see how close CCZ’s assets are to Corazon’s (ASX: CZN) projects. Interestingly, CZN recently significantly expanded its cobalt and copper anomaly.

CCZ is confident it can repeat CZN’s success as it looks to boost its $21 million market cap and take advantage of current sentiment in the cobalt market.

However, it is early stages here and investors should take all publicly available information into account and a cautious approach to their investment decision in this stock.

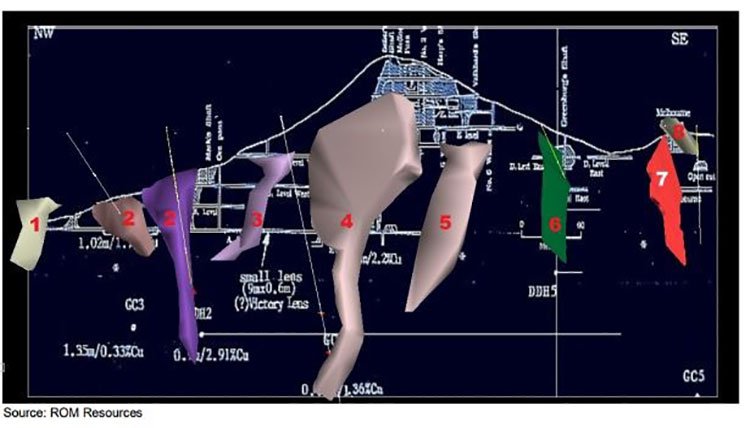

Through 3D modelling conducted by ROM Resources, the Jackaderry South Prospect was found to be the fastest route to delivering a JORC compliant resource for copper-cobalt-zinc. The 3D JORC modelling highlighted the potential to develop an open pit mine, keeping extraction costs moderate.

Here is the 3D model:

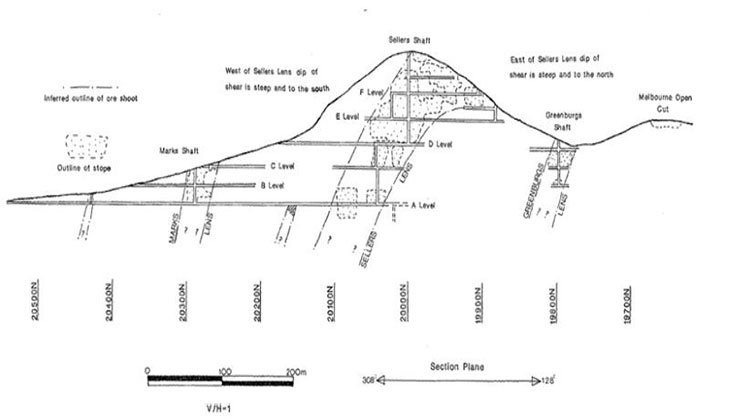

CCZ has been working predominantly off historical data. The following cross section map shows previous workings projected on a vertical plane.

Importantly, legacy mining in the 1900s only went down to 85m. Not too far at all. And it was drilled using manual labour, meaning this has always been high-grade. Here’s a look at the Cangai Mine entrance and the copper smelter and tramway.

In the last 30-40 years, one hole in particular intersected near vertical ore shoots at 230m, which again exhibited significant mineralisation.

Furthermore, Cangai has always attracted the attention of majors, the last of which was CRA before being taken over by Rio Tinto.

CRA abandoned the project during the recession in the 1990s, but clearly had some very positive results and data which CCZ is now capitalising on.

The region is proven to have significant cobalt mineralisation and core samples tested by ROM Resources exhibits iron sulphide which also carries cobalt mineralisation.

With its first high-grade JORC under its belt, CCZ will now turn its attention to JORC Resource number two, as well as follow up on its business plan as it looks to sign agreements with third party processors within close distance of the projects to expedite production and cashflow generation.

CCZ’s competitive advantage

CCZ has found itself with a competitive advantage that will no doubt play a role in its overall ambitions.

This advantage is all down to its supergene ore, which is a highly rare. Desktop research has confirmed supergene ore present with up to 35% copper .

What does this mean?

The discovery of supergene ore implies the presence on an enriched copper resource and is a material point of difference from numerous rivals.

Essentially, because supergene ore processes or enrichment are those that occur relatively near the surface as opposed to deep hypogene processes, this could be a game changer for CCZ.

Importantly, the ore occurred close to surface, passed into chalcocite ore with a similar grade below surface, which translates into significant exploration upside.

As mentioned above, there are similarities here to the $904 million Sandfire Resources.

CCZ is hoping its supergene ore delivers it a similar strategic competitive advantage to Sandfire as the DSO to end-users can becomes a reality. This certainly isn’t out of the question with the company close to infrastructure with sealed roads that link directly to Newcastle Port.

If this occurs it would imply securing higher operating margins, which fits nicely with CCZ’s business plan.

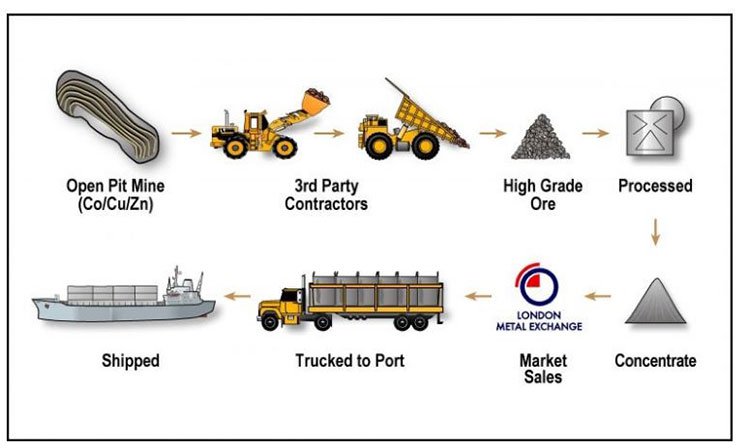

A quick look at the business plan

CCZ has a clear strategy.

It’s a plan designed to ensure costly and time-consuming requirements to build facilities onsite are avoided, giving CCZ a significant strategic point of difference from its many rivals.

The plan looks like this:

The following workflow model gives you further indication of how CCZ expects to fulfil its goals:

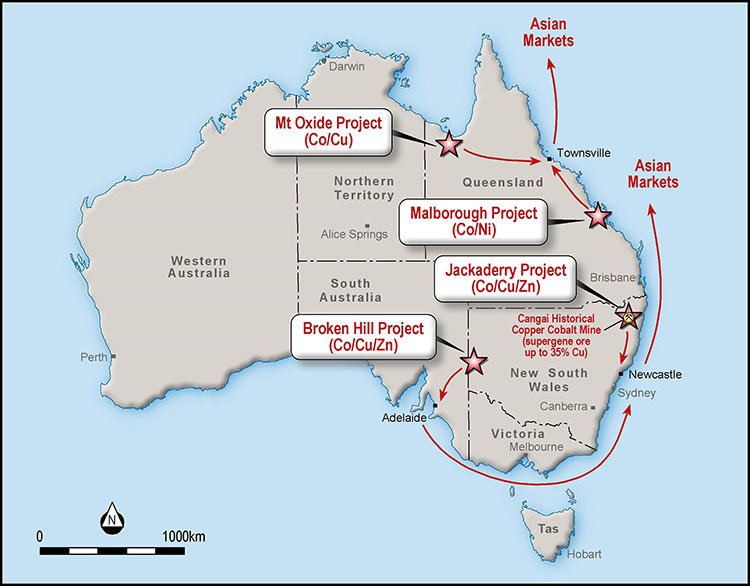

With this workflow model in mind, the map below highlights the location of CCZ’s projects and path to Asian markets.

Back to Broken Hill

Whilst its main focus is on Cangai, Broken Hill will be the next Resource off the rank, and as with Cangai, a preliminary report by ROM Resources highlights JORC modelling is focused on the southern part of the tenure which exhibits high grade zinc mineralisation.

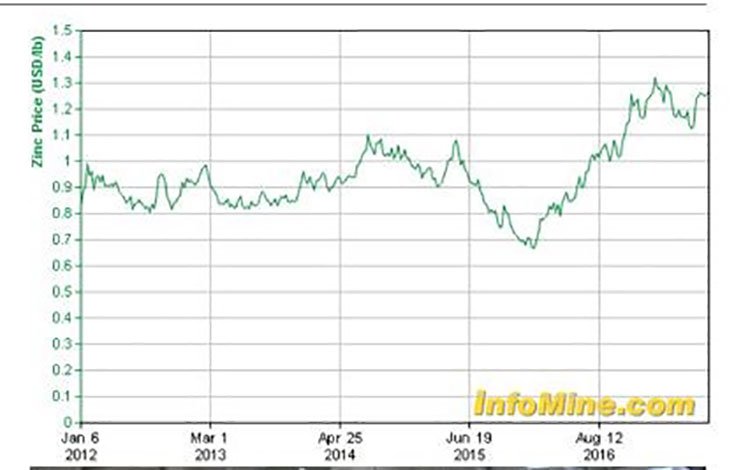

Broken Hill gives CCZ a primary zinc deposit at a time when there is supply deficit and the zinc price continues to reach new heights.

2017 has seen mine shutdowns, weather related outages and a reduction in global inventories, which is keeping upward pressure on prices as seen in the chart below.

Of course commodity prices do fluctuate and caution should be applied to any investment decision here and not be based on spot prices alone. Seek professional financial advice before choosing to invest.

Given these macro factors, CCZ is looking to capitalise on current events and open up a new supply chain.

Acquisition could extend Resource

CCZ is taking an aggressive approach to expanding its overall mineralised footprint and prospective JORC compliant Resource sizes across its Australian projects.

Backed by an upcycle in base metals, CCZ looks to be pulling out all the stops to prove up its JORC Resources and fast track production.

Recently, CCZ signed a binding Heads of Agreement with Total Iron Pty Ltd , which owns five highly prospective copper-cobalt-zinc-nickel project areas in NSW and QLD, to expand CCZ’s mineralised footprint.

The acquisition would give CCZ a total of 11 project areas in four geographic locations and would enhance its overall mineralisation footprint and potential size of JORC compliant Inferred Resources presently being modelled.

Other benefits include:

- The delivery of two complementary project areas to Jackaderry and Mt Oxide respectively, and bridgehead into north-east Queensland.

- Create a scalable operation, with four high quality projects close to excellent land transportation infrastructure, third party processors and proximity to ports to tap into Asian markets.

- Reshape the JORC modelling priority to Cangai Mine, enlarge Jackaderry South prospect then Broken Hill using legacy data, followed by Mt Oxide and Marlborough which require drilling.

- Doubling the Jackaderry South project area and potential mineralised Resource size.

Beyond Cangai

The acquisition of Total Iron, brings into play CCZ’s other assets. Whilst Cangai benefits with an increase in potential Resource size and upside potential, the Mt Oxide Project Group will also benefit from the acquisition of Total Iron. Total Iron’s Alpha Cobalt Project lies south west of CCZ’s Big Oxide North and Hill of Grace tenures which make up Mt Oxide and enhance the mineralisation footprint and prospective Resource size in an area well-known for copper-cobalt.

A drilling programme will begin at Mt Oxide in Spring, which will facilitate modelling a JORC Compliant Resource.

The final piece of this particular puzzle is the Marlborough Project in Queensland. Marlborough comprises three prospects located northwest of Gladstone in an area known for high-grade cobalt-nickel systems.

According to Queensland’s Department of Natural Resources and Mines, legacy data shows the area covered by the Marlborough Project and Queensland Nickel contains proven and probable reserves of 48.7Mt at 0.94% nickel and 0.06% cobalt with a total Resource of 70.8Mt.

There’s a lot of upside for CCZ with its Marlborough play, but this is an early stage prospect and part of its longer term plans.

The big plan

By enlarging its mineralised footprint, CCZ has been able to simplify its tenure structure into four groupings: Jackaderry, Broken Hill, Mt Oxide and Marlborough.

Three projects are already highly prospective for cobalt-copper-zinc and to a lesser extent nickel.

As such, with one high-grade JORC Resource now in the bag, CCZ is intent on proving up two more JORC compliant Inferred Resources in quick succession.

Broken Hill will follow Cangai (next week) and Mt Oxide will follow later in the year from a maiden drilling campaign.

Detailed desktop work will commence at Marlborough shortly to ascertain key targets for a drilling campaign.

CCZ is also determined to begin liaising with third party processors within range of Cangai to help expedite end-product to market via the LME.

The next few months will be flush with catalysts including the announcement of further JORC Resources that could play a big role in helping to re-rate this $18.7 million capped company.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.