KMT Shines a Spotlight on ASX Copper Corner From World-Class Kalahari Copper Belt

Published 27-FEB-2018 10:00 A.M.

|

14 minute read

Hey! Looks like you have stumbled on the section of our website where we have archived articles from our old business model.

In 2019 the original founding team returned to run Next Investors, we changed our business model to only write about stocks we carefully research and are invested in for the long term.

The below articles were written under our previous business model. We have kept these articles online here for your reference.

Our new mission is to build a high performing ASX micro cap investment portfolio and share our research, analysis and investment strategy with our readers.

Click Here to View Latest Articles

The Next Small Cap presents this information for the use of readers in their decision to engage with this product. Please be aware that this is a very high risk product. We stress that this article should only be used as one part of this decision making process. You need to fully inform yourself of all factors and information relating to this product before engaging with it.

Small cap explorer, Kopore Metals (ASX:KMT), is hoping to breathe new life into the ASX’s copper corner as copper prices surge in parallel with building demand and tightening supply.

KMT is doing this through its recently acquired Kopore Copper Project, situated in one of Africa’s most highly ranked mining investment districts: Botswana’s prospective yet under-explored southern Kalahari Copper Belt.

The Kopore Project spans some 7,891 square kilometres directly alongside a knot of major peers, including the $100.5 million-capped MOD Resources Ltd (ASX:MOD) and the privately owned Cupric Canyon Capital, LLC.

This project positions KMT as the third major player in the belt alongside these global heavy-lifters. Not bad for an early-stage $16.5 million-capped explorer.

Here, KMT boasts a dominant ground position with 100% owned tenements that adjoin MOD’s tenure.

That’s some serious highlights already:

-

A $16.5 million capped company

-

Next door to the $100 million capped MOD

-

MOD price target currently $204 million

-

100% owned tenements

-

With the same geophysics and structures.

Since snapping up its tenements back in November via its acquisition of Global Exploration Technologies — and changing its name from Metallum Limited (ASX:MNE) — KMT has been making quick-footed progress on an initial series of sharply focused exploration activities.

KMT has in this short period of time, continued to demonstrate increasing exploration prospectivity across its licences through each exploration program, identifying ground geophysical conductors and soil anomalies forming immediate targets.

It is, however, still an early stage operating in a high-risk region, so investors should seek professional financial advice if considering this stock for their portfolio.

The most recent news on this front shows distinct promise — as KMT announced this week, a recently completed maiden airborne and electromagnetic (AEM) survey has identified multiple EM conductor zones that form part of a regionally interpreted, large domal structure.

These zones range from shallow depths below surface to deeper targets of more than 250 metres, and zones of conductors up to four kilometres in strike length, located across the Ghanzi West 1 (GWD1) prospect.

On top of that, reprocessing of newly acquired regional magnetic airborne raw data and a recent field geological reconnaissance program has confirmed the presence of the targeted D’Kar formation over the GWD1 target.

Intriguingly, this formation is known to host most of the mineralisation on the Kalahari Copper Belt, including Cupric Canyon Capital’s neighbouring Zone 5 and MOD’s T3 copper-silver project.

Further targets are being refined as we speak, and exploration works are set to begin in March — just weeks away.

This exploration programme will include targeted ground geophysics and soil geochemical surveys, aiming to further enhance drill targeting, upon government approval.

This will likely translate into steady news flow from KMT in the weeks and months ahead as everything falls into place.

To top that off, KMT is backed by a confident in-country management team with deep knowledge of the area to advance exploration and development of its considerable assets.

And its timing is apt, to say the least. After finishing last year with a strong rally, current copper sentiment is decidedly positive, driven by considerable demand from China, the world’s largest consumer of copper.

As we steadily transition into an electric vehicle-powered future and increasingly focus on renewable energy sources, global copper demand is set to surge exponentially over the coming 20 years.

Given its prime position in a rapidly emerging African district, strong exposure to quality copper, and a jam-packed exploration schedule set to kick off in a matter of weeks, KMT is a company to track closely.

With $3 million in the bank, a low enterprise value of $15.7 million and a tiny $16.5 million market cap, this ASX junior could be a salient entry point into a commodity corridor that’s poised for further heights as copper demand spikes.

Catching up with:

![]()

Kopore Metals (ASX:KMT) is an emerging explorer with an eye on the thriving copper rally and an unflinching sense of focus.

KMT’s strategy is simple: to progress its aggressive exploration campaign at the rapidly emerging Kalahari Copper Belt and to fashion itself into the next major ASX copper player.

The ASX retains a small corner of listed copper explorers and developers, with a conspicuous lack of quality copper exposure, presenting an excellent opportunity for a forward-focused copper junior to shake things up.

With limited discoveries and increasing demand very much in its favour, this could be just the setting for KMT’s emergence as a significant copper contender.

KMT’s acquisition of the Kopore Copper Project last year was a considerable game-changer.

And with this acquisition has also come a freshly refurbished management. Kopore’s well-muscled management team, which includes Grant Ferguson, Tim Goldsmith and David Catterall, all of whom have extensive experience in southern Africa, have joined KMT’s ranks. Their combined CV boasts an expansive track record of exploration success resulting in major new mines in southern Africa and the Kalahari Copper Belt.

Notably, the Botswana-based Catterall, who previously held geologist and exploration roles with Cupric Canyon, the dominant player on the Kalahari Copper Belt, and has 30 years under his belt in the resource industry.

Bearing that in mind, before we look in more detail at the latest development to transpire at Kopore, let’s take a moment to set the scene...

The setting

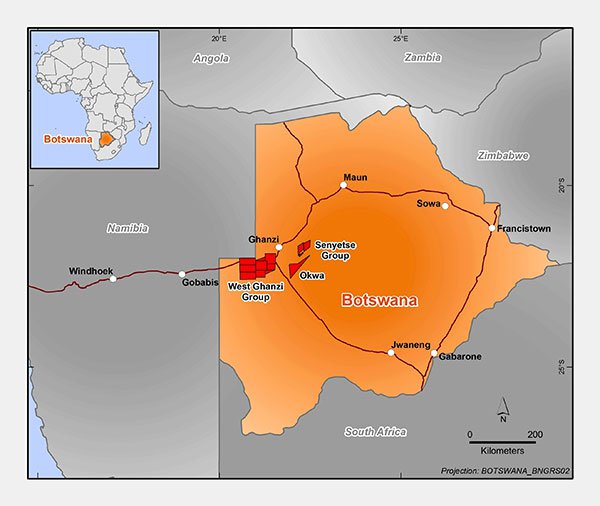

The Kopore Copper Project spans some 7,891 square kilometres in the western part of the Kalahari Copper Belt in north-west Botswana.

KMT’s tenements cover three key areas of the belt: the Ghanzi West Group, Okwa and the Senyetse Group.

Setting counts for a lot here. The Kalahari Copper Belt is an emerging, relatively underexplored, world-class copper province with total reported Mineral Resources of over 7Mt of contained copper (14 billion pounds copper) and 260 million ounces of contained silver.

Botswana isn’t just an appealing setting for its geological potential, but is also ranked second in the Fraser Institute Mining Investment Attractiveness Ranking for Africa, as well as eighth in the world.

An establishing shot, to give you a broad idea of where KMT has set its sights:

Recent discoveries here have dramatically improved geological understandings of this belt and amplified new targets, which means that KMT’s course of action will be precise and purposeful as it follows on from its maiden exploration works.

As we’ve mentioned, KMT is also in close range to some major neighbours, including the aforementioned MOD, whose 36 million tonne T3 project sits at 1.14% copper. MOD recently released positive pre-feasibility study results, demonstrating a profitable initial open cut operation at T3.

It was also the subject of a recent broker report conducted by Argonaut which has slapped a $204 million price target on the company.

It should be noted that broker projections and price targets are only estimates and may not be met. Those considering this stock should seek independent financial advice.

Given how similar the two projects are, KMT would be hoping for similar traction in the near future.

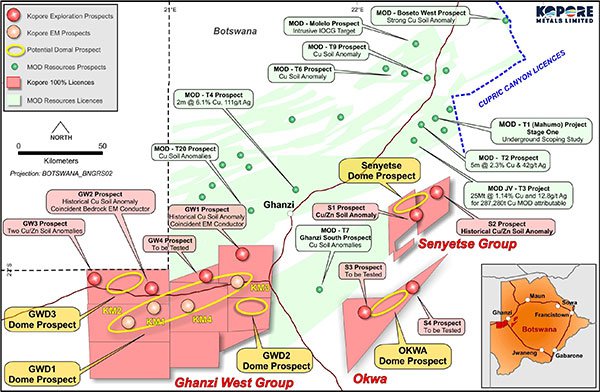

In the map below, you can see where KMT’s exploration targets are situated in relation to its peers:

As you can see, KMT is practically rubbing shoulders with MOD, with adjoining tenure. MOD is an especially noteworthy player here for a number of reasons.

Over the last couple of years, MOD has been the darling of the Kalahari Copper Belt, rising from some $5 million in market cap to the $100.5 million it is today.

The work of MOD has also helped to establish a new interpretation of the southern Kalahari Copper Belt, unveiling significant prospectivity in the region extending directly into Kopore’s ground.

KMT is hoping for similar success. Today, KMT is capped at a mere $16.5 million, but should the interpreted geology at Kopore result in a copper discovery, its micro-cap days could become a distant memory.

Meanwhile, also neighbouring KMT is the North West Transmission Grid (NWTG) Project, which commenced field activities this month, as this Mmegionline article explains:

Importantly, the NWTG will provide grid power along the Kalahari Copper Belt, and is expected to be completed in 2019-2020. This, in turn, will provide significant benefits to potential operators along the belt, including potential operating cost reductions... which bodes very well for explorers like KMT.

The latest at Kopore: multiple electromagnetic targets identified

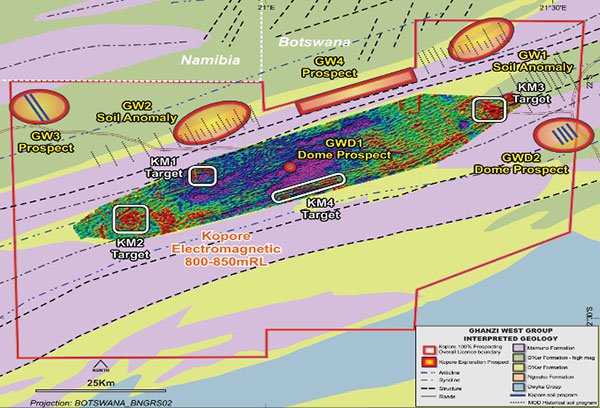

KMT’s recently completed airborne magnetic and EM survey covered an area of some 1,091.7 square kilometres, and was conducted by the South Africa-based NRG Exploration CC using tried and tested techniques that have proven successful in delineating copper mineralisation.

You can see these activities afoot in the images below:

Encouragingly, initial airborne results have highlighted four high-priority electromagnetic (EM) conductor zones across the GWD1 dome prospect, as well as identifying a number of other regional targets for follow up.

These targets comprise multiple interpreted potential conductors within zones up to four kilometres in strike length and from less than 50 metres below surface to deeper conductors.

Promisingly, initial interpretation indicates the presence of anticlinal and synclinal folds within the overall GWD1 prospect area. As the GWD1 prospect AEM survey extends over a very large area of some 1,091.7 square kilometres, KMT believes that such a substantial area could hold anticlinal and synclinal folds, with both styles carrying potential for copper mineralisation, as evidenced in other major copper deposits along the Belt.

KMT has now confirmed that the GWD1 prospect is bound by major northeast/southwest faults and can be interpreted as an additional structural corridor on the Kalahari Copper Belt — something that also bodes nicely in terms of potential mineralisation.

Initial modelling of these ranked conductor zones indicates the presence of high and low and angle conductors, reflecting the varying geological structural conditions within the underlying lithologies.

The GWD1 dome survey, showing reinterpreted geology and exploration prospects

On top of this recent airborne survey, an airborne regional magnetic reprocessing and ground reconnaissance program has helped KMT to refine its exploration targets.

This reprocessed data has identified a historically drilled water borehole within the GWD1 prospect area, showing minor pyrite mineralisation within the drill cuttings, this could be useful in sharpening up KMT’s future detailed targeting.

Although, the company still has a long way to go to meet its targets and thus investors should continue with a cautious approach when considering this stock for their portfolio.

What next?

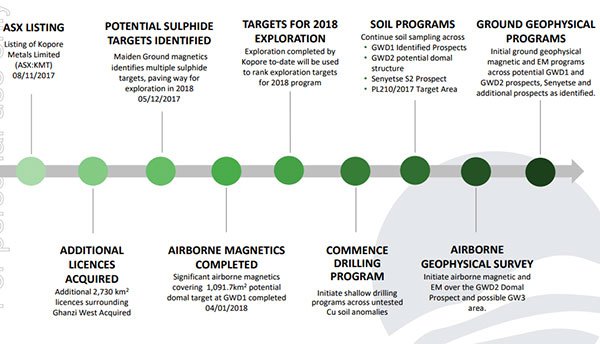

Here’s a look at KMT’s timeline since its pivotal acquisition last year, up until now:

As you can see, that’s a steady, regular flow of news for an ASX small cap explorer to sink its teeth into, and this will continue as KMT moves forward in the weeks and months to come.

KMT’s exploration to date continues to validate the geological model and high-level potential of this underexplored corner of the Kalahari Copper Belt, and things are set to ramp up further.

Based on the initial results of its maiden exploration program, KMT has now reassessed its portfolio prospects and made the identified GWD1 AEM targets its central priority, with the plan to begin ground geophysical and soil sampling exploration programs on these targets in the near future.

KMT is also investigating the potential for T3-esque geometry, and will be conducting detailed ground geophysical programs over each of its identified EM prospects.

Furthermore, KMT will continue to review survey results and integrate the results of this review with its further planned ground reconnaissance programs and drilling.

The company has also designed detailed ground geophysical programs to follow up selected prospects, which will hopefully help refine the targeting process and establish a better understanding of potential geometry. This, in turn, will be used for exploration drill targeting.

Exploration works, including targeted ground geophysics and soil geochemical surveys, are planned to begin in March — a matter of weeks from now — aiming to further enhance drill targeting.

Drilling will kick off once government approvals have been received. And at around the same time, final AEM survey results are expected back.

In short, KMT has plenty to keep it busy, much of which could also translate into share price catalysts.

A major player in the belt

With 100% ownership over 7,891 square kilometres within a major interpreted mineralisation corridor and a cluster of immediate targets, KMT has on its hands a promising opportunity for what could well be a Tier 1 discovery.

This acquisition provides an excellent opportunity to drive significant growth for KMT, especially given its pre-existing exposure to copper.

KMT sits as the third major player in the Kalahari Copper Belt. These are still early days, but there’s a lot of promise ahead for this soon to be very busy copper junior.

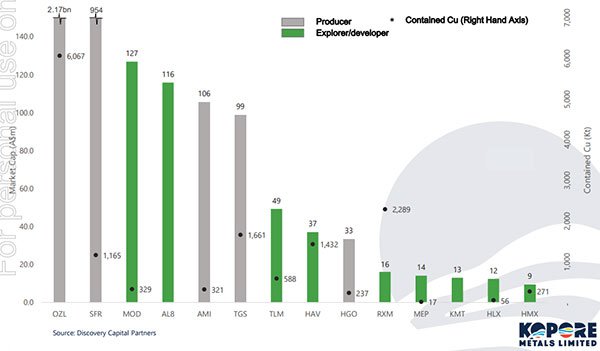

The chart below gives you an idea of how KMT stands, comparing KMT market cap and volume of contained copper to that of its peers:

There’s also significant headroom for growth among KMT’s ASX peers, with leverage to multiple exploration targets.

And with copper demand on a high, now could be a pertinent time to look for the rust-coloured metal in one of Africa’s most highly ranked mining districts.

Speaking of which...

A copper renaissance?

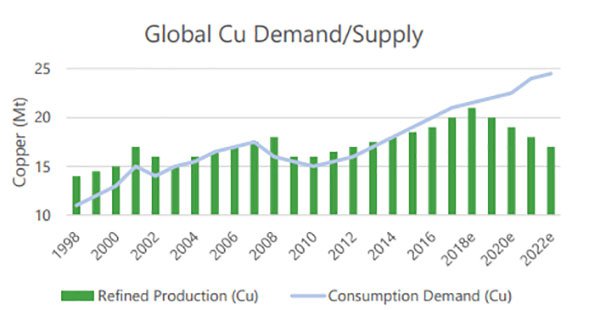

As the market widely acknowledges a clear and growing supply deficit, copper is experiencing a hefty resurgence.

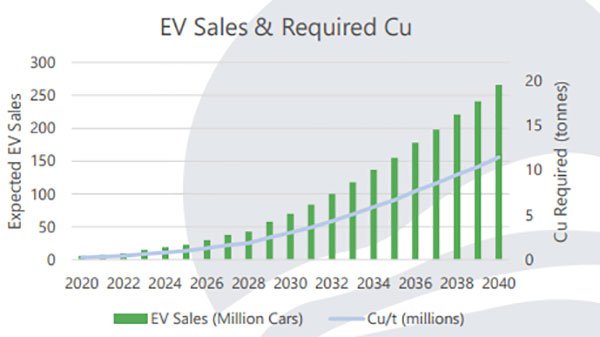

For one, it’s set to capitalise on the Tesla-powered electric car revolution, with the growing number of electric vehicles hitting roads set to fuel a nine-fold increase in copper demand from the sector over the coming decade.

According to a study commissioned by the International Copper Association (ICA), conducted by IDTechEx, electric or hybrid cars and buses are expected to reach 27 million by 2027, up from 3 million last year.

This increase is set to raise copper demand for electric cars and buses from 185,000 tonnes in 2017 to 1.74 million tonnes in 2027.

EVs use a substantial amount of copper in their batteries and in the windings and copper rotors used in electric motors. A single car can have up to six kilometres of copper wiring, according to the ICA.

This bodes very nicely for KMT, but it’s not the only factor working in copper’s favour...

When it comes to the current copper sentiment, coverage like this speaks eloquently:

As headlines like these suggest, a number of elements are at play here in driving copper prices.

For instance, supply disruptions at some of the world's biggest mines, including BHP's Escondida mine in Chile last year and ongoing strike action at Freeport McMoRan's Grasberg operations in Indonesia, are also boosting the copper price.

However at the same time, we should point out that commodity prices can fluctuate, so caution should be applied to any investment decision and not be based on commodity prices alone.

Copper is poised to continue tracking higher as current copper mines become exhausted, adding to the current supply deficit.

Given all of this, it seems like KMT could very well be in the right place, at the right time.

A bright future

If this ASX copper junior can manage to get a commercial supply up and running in the Kalahari Copper Belt, it could stand to significantly tap into both these discordant supply-demand dynamics and the increasingly fast-paced EV boom.

Things are expected to seriously ramp up shortly at Kopore, with further exploration kicking off next month, and here at the Next Small Cap , we’ll be sure to keep our ear to the ground.

General Information Only

S3 Consortium Pty Ltd (S3, ‘we’, ‘us’, ‘our’) (CAR No. 433913) is a corporate authorised representative of LeMessurier Securities Pty Ltd (AFSL No. 296877). The information contained in this article is general information and is for informational purposes only. Any advice is general advice only. Any advice contained in this article does not constitute personal advice and S3 has not taken into consideration your personal objectives, financial situation or needs. Please seek your own independent professional advice before making any financial investment decision. Those persons acting upon information contained in this article do so entirely at their own risk.

Conflicts of Interest Notice

S3 and its associated entities may hold investments in companies featured in its articles, including through being paid in the securities of the companies we provide commentary on. We disclose the securities held in relation to a particular company that we provide commentary on. Refer to our Disclosure Policy for information on our self-imposed trading blackouts, hold conditions and de-risking (sell conditions) which seek to mitigate against any potential conflicts of interest.

Publication Notice and Disclaimer

The information contained in this article is current as at the publication date. At the time of publishing, the information contained in this article is based on sources which are available in the public domain that we consider to be reliable, and our own analysis of those sources. The views of the author may not reflect the views of the AFSL holder. Any decision by you to purchase securities in the companies featured in this article should be done so after you have sought your own independent professional advice regarding this information and made your own inquiries as to the validity of any information in this article.

Any forward-looking statements contained in this article are not guarantees or predictions of future performance, and involve known and unknown risks, uncertainties and other factors, many of which are beyond our control, and which may cause actual results or performance of companies featured to differ materially from those expressed in the statements contained in this article. S3 cannot and does not give any assurance that the results or performance expressed or implied by any forward-looking statements contained in this article will actually occur and readers are cautioned not to put undue reliance on forward-looking statements.

This article may include references to our past investing performance. Past performance is not a reliable indicator of our future investing performance.